To access this post, you must purchase Quarterly Subscription or Yearly Subscription

Upgrade Now

Whether it’s a black swan or a white rhino, the Covid-19 Pandemic will go down as one of the major events in world history.

In my mind, the question that remains is whether Covid-19 is remembered more for the deaths it has caused or the financial and social chaos which could follow?

Personally, if I had to choose, my guess would be that history will look back at the Covid-19 crisis as the precipice of something much bigger.

Clearly, the world financial system has been pushed to its limits, as the U.S. Federal Reserve’s pledge of QE Unlimited really makes you wonder where this is all headed.

On the social side of things, there have been many troubling developments, from the Canadian government’s attack on free speech to India’s Aarogya Setu tracking app, which allows the Indian government to track its users.

It’s a brave new world.

With that said, the case for higher gold prices has literally never been better than it is today.

Although higher gold prices spur thoughts of grandeur among many gold bugs, higher gold prices do come with the caveat of chaos.

The late Richard Russell said, and I’m paraphrasing,

“In the next crisis, it isn’t who makes the most, but who loses the least.”

Given the circumstances, he may very well be right – a sobering thought.

Today, I have for you an interview with one of the resource sector’s best, Mark O’Dea, who is the Founder and CEO of Oxygen Capital.

In the interview, we cover a number of topics, including the investment thesis for PureGold, which is in the midst of constructing its PureGold Red Lake mine in Northern Ontario.

Enjoy!

Brian: The Covid-19 crisis has swept over the world the last few months, shutting down economies and forcing us into uncharted territory both economically and socially. Governments have pledged unprecedented amounts of money to repair the damage, but uncertainty about the future still remains.

In a 1959 speech, John F. Kennedy said,

“The Chinese use two brush strokes to write the word ‘crisis.’ One brush stroke stands for danger; the other for opportunity. In crisis, be aware of danger – but recognize the opportunity.”

In your opinion, today, what danger should people be aware of and, secondly, where is the opportunity?

Mark: Well, thanks Brian. I think the danger is already baked into the reality that we’re all living right now. Stocks have been crushed, economies are struggling, danger levels remain high and people are on high alert. Whether stocks fall lower, testing the lows of a few weeks ago or not, remains to be seen. It kind of feels like that’s not the case, but who knows? I think throughout this, what’s emerged as an opportunity, a sort of counterpoint to all that risk and crises, is that gold is looking really constructive and is in a very good place right now. So, it’s done what it’s meant to have done in the sense that it’s behaved really well. If you look at its chart, it’s up 33% over the past year and it’s up 13% year to date in the face of this massive financial crisis, and it’s trading at or above US$1700 an ounce.

As governments continue to print trillions of dollars to stabilize the economy with interest rates near zero and debt levels through the roof, gold has reacted to that and has adjusted upwards very nicely. Printing all this new money inevitably leads to serious reduction in the future purchasing power of a dollar. Owning gold, which is rare and intrinsically valuable, as opposed to a paper dollar, is a way to preserve the purchasing power of your money. So, in my experience, having gold as an allocation in your portfolio is a sensible thing to do.

There are great opportunities that exist in the gold equities right now, and what’s compelling from an investment thesis is that we’re seeing operating margins increase dramatically with this rise in gold price. So, if a company, for example, was making $300 an ounce in margin a year ago, they’re now making $600 or $700 an ounce and that bump in profitability goes straight to their bottom line. That massive margin expansion isn’t yet priced into the equity valuation in my opinion. So, I think there’s a pretty interesting opportunity to capture there. It gets even more pronounced for Canadian gold mining companies like Pure Gold Mining (PGM:TSXV), for example. Because the Canadian dollar has weakened relative to the US dollar, gold is now trading at all time highs in Canadian dollar terms. Gold is hovering around $2,400 Canadian dollars per ounce. It really is incredible.

So, for a near term Canadian producer like Pure Gold, where your costs are in Canadian dollars but you’re selling a product in US dollars, it translates into huge margin expansions at the operation, so profitability goes way up.

Brian: Recently, Barrick Gold announced that the Government of Papua New Guinea would not be extending Barrick’s Special Mining Lease on their Porgera gold mine.

The nationalisation of assets is a risk which miners in the developing world always have to consider.

My question for you is do you believe there is more political risk in the developing world today, given the economic calamity we are facing globally? Please explain.

Mark: I think it’s inevitable that risks in developing countries have gone up. The economies of developing countries are at risk of being completely wiped out or at least pushed back 20 or 30 years because of this crisis. I firmly believe that this inevitably leads to increased chances of expropriation of mining projects. It becomes a matter of survival.

In contrast, in countries like Canada and the United States for example, things are quite a bit different. Big mining and development projects become a key part of the engine for re-stimulating the economy through all the direct and indirect benefits and the increased tax base created. Getting people back to work in high paying jobs goes a long way to helping a nation recover. So my prediction and hope is that we’re going to see big resource development projects multiply and come online quicker as a stimulant for recovery in developed countries.

Brian: A quick binary question for you, will gold be trading above US$2,000 per ounce by the end of 2020, yes or no?

Mark: I rarely make predictions around commodity price because I’m always wrong. But given the macro environment that we are in for gold, it feels like a perfect storm. So, I wouldn’t be at all surprised to see gold reach US$2,000 an ounce this year.

Brian: Without a doubt, the case for gold has never be stronger than it is today. Given this, I personally see tremendous upside potential in owning gold equities, especially the best of the best juniors. Oxygen Capital has a great stable of companies, all of which have varying degrees of exposure to precious metals.

To me, PureGold (PGM:TSXV) stands out from the rest given its stage of development, as it has commenced detailed engineering, procurement and construction of its PureGold Red Lake mine.

First, could you give us an overview of the Red Lake Gold Camp and why is having property within the Red Lake Gold Camp so valuable?

Mark: There are 30 million reasons to like Red Lake, and by that I mean there have been 30 million ounces of high grade gold produced in the camp over the past +80 years. It’s become world famous for some of the highest grade gold ever produced – anywhere. It’s a place where Tier one companies are born and bred. For example, it turned Goldcorp into what it became after the discovery of the famous High Grade Zone in the late 1990s. It was Placer Dome’s bread and butter and jewelry box for decades. Red Lake exists as a place because of mining, so as a location, you couldn’t ask for any better. Many of us at Pure Gold cut our teeth in Red Lake. And frankly I think that is a key attribute of our Company. If you are building Canada’s next gold mine in Red Lake, you want a team with significant Red Lake experience. For example, Darin Labrenz, our President and CEO worked in Red Lake for 10 years and was Chief Geologist at Placer Dome’s Campbell Mine. Phil Smerchanski, VP Exploration and Chris Lee, Chief Geoscientist, both worked extensively in the Red Lake camp for Goldcorp and other companies. I consulted for Goldcorp in Red Lake, early in my career and started my first Company called Fronteer Gold with an initial focus on Red Lake, backed by Placer Dome and Rob McEwen. Rob Pease, one of our directors, was General Manager Exploration for Placer Dome where he was responsible for Canadian exploration, including Red Lake. Finally, Maryse Belanger, also a Director, was a Senior VP Technical Services for Goldcorp, whose responsibilities included the Red Lake Mine Complex.

So, we have all spent years working at, and figuring out other people’s mines in Red Lake, and have more on the ground experience in the camp than any other group in the world. It feels so exciting to now be on the cusp of running our own mine and being the next chapter in the evolution of this incredible place. It feels like coming home.

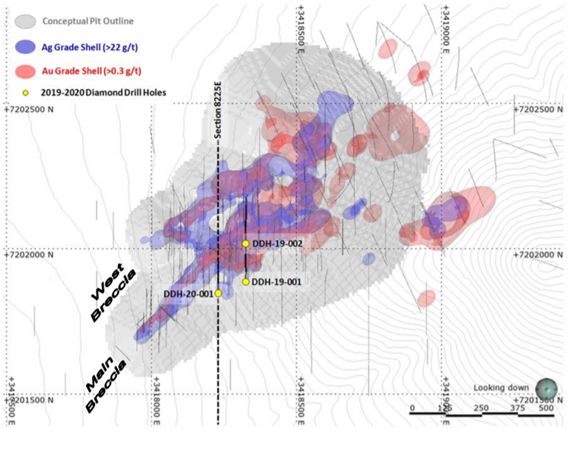

What I have also learned is that not all geology is created equally in Red Lake. And we control (100%) of a continuous ten kilometre long stretch of some of the most fertile gold rich geology in the camp. We feel strongly that despite having already defined well over 2 million ounces of gold, and being the 5th highest grade gold mine in Canada, we have just barely scratched the surface.

Brian: Secondly, could you give us an overview of the current investment thesis for PureGold?

Mark: The first investment thesis really revolves around near-term production and cash flow into a rising gold market. The second, and equally important theme is grade, resource growth and the scalability of the mine itself. So let’s start with the first one, the near-term cash flow. We are coming out of what’s traditionally viewed as a fairly dull period in any company’s evolution. That is the construction phase of a mine. We are nearing completion of construction now and there is clear visibility to first gold production. We can see the finish line and we anticipate pouring gold before the end of this year. What typically happens during this period is a Company’s valuation begins to re-rate upwards from a developer to a producer. For example, when you look at what junior producers are trading at today, they are valued at roughly one times their Net Asset Value (1 x NAV). Currently, Pure Gold is trading at much lower than that. So, as we get our Phase 1 mine plan into production and in turn demonstrate that we can quickly scale up to even higher production rates, I really believe there is a valuation gap that is going to get filled. Layer onto that the strong operating margins that come from gold being at roughly $2,400 CAD per ounce, and you have a project that generates an additional $C680M of cash flow compared to our feasibility study just 12 months ago. This type of margin expansion isn’t factored into our equity valuation at all.

Brian: Finally, where is the upside potential – Is the deposit open at depth? Is there potential for discovery on other targets within the project’s land package?

Mark: What’s really unique about these types of deposits is that they pack a huge punch in a relatively small footprint and they’ve got very, very deep roots; they continue for kilometers at depth. The perfect example of this is the Red Lake Mine Complex up the road. It has produced 20 million ounces and has been mined down to 2.5 km depth. We have exactly the same geology and potential at Pure Gold, with the same opportunity for growth. Our orebody is about 7 km long currently and has only been drilled off in places to about 1km depth. It is literally open in all direction. And I feel we’ve barely scratched the surface. The real prize is still yet to be found. We have already defined two and a half million ounces of gold at ~9 g/t from 1.3 million meters of drilling. So it is exceptionally well understood geologically. We know mineralization continues at depth because we have intersected it in drill holes down to 2.1 km depth. We know It keeps going. So in my opinion, by extending the deposit down to the depths that they’re mining at the Red Lake complex up the road, you can see the potential for at least another five million ounces here. It is important to me that when investors look at Pure Gold they don’t just see the current reserves and resources. But rather, they see this as a multi-generational asset that is going to keep growing in size with ongoing drilling. Pure Gold is a big part of the future of Red Lake and we are on the cusp of starting a whole new chapter in this world class mining region.

Brian: Formal and informal mentors have made a tremendous impact on my life. I can honestly say that without their influence I wouldn’t be where I am today.

What is the best piece of advice a formal or informal mentor has given you?

Mark: One piece of advice would be to stick to your knitting and trust that value will come. It’s easy to get distracted in this business. But I do believe that sticking to your knitting and playing the long game is the way to go. Especially if you are lucky enough to be sitting on a project as special as the one we have at Pure Gold. And that’s advice that was given to me by some wise mentors, and it’s certainly served me well. There are no overnight successes in this business. It might look that way from the outside looking in, because values crystallize in an instant in a takeover or in an exciting discovery. But preceding that moment, there are usually 5 or 10 years of incredibly hard work. A second piece of advice would be that you can’t do it all yourself and you need a team you can trust. Surround yourself with people who are smarter than you. Let your talent run and trust them.

Brian: If you could offer a piece of advice to your 20-year-old self, what would it be?

Mark: I was 34 years old when I became CEO of my first company, Fronteer Gold. So I will give my 34 year old self some advice. And that is “comparison is the thief of joy”. I think it’s a useful piece of advice because there’s always a stock or a company that’s higher or lower than yours for reasons that don’t make any sense at all. And they may never make any sense. Don’t obsess about it. You can let it motivate you and learn from it, but you must keep your eyes focused on what you can actually control and focus on doing everything to the best of your ability to create fundamental value.

Next would be, raise more money than you think you’ll need because the companies that do the best in this business do not do it by raising half a million dollars at a time. That gets you nowhere. You want to raise enough money to get meaningful work done and take a project from one milestone to the next so you can unlock value. The companies that have the best valuations are the ones with a healthy treasury giving them enough working capital to make real progress.

Brian: Finally, at the end of our last interview, you left us with a very timely quote from Miles Davis.

“Time is not the main thing. It’s the only thing.”

Do you have any words of inspiration for today’s investors?

Mark: I would say do your homework. It’s easy to jump on the momentum train. Do your homework, look for transparency in companies. Look for companies that are going to take you along with them through the steps in their evolution, from resource to economic studies to permitting and so on, rather than companies who lack that transparency.

To take a quote from Abe Lincoln,

“If I had 6 hours to chop down a tree, I would spend 4 hours sharpening my axe.”

Spend 4 hours sharpening your axe and do your homework on the companies that you are going to invest in. Make sure they are backed by good people, with a solid track record, who have skin in the game and who have good projects in good places.

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review Premium

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria.

NOTE: This interview was first published for Junior Stock Review Premium readers on April 2, 2020. Become a today and get my best investment ideas, market commentary and interviews first.

Over the course of my life, there have been a number of people who have made a significant impression on me.

Some of these people made an impression before I’d even met them.

I have mentioned before that my introduction to gold and what it means to be a libertarian started with Doug Casey. I had never contemplated the idea of sound money or the short falls of government before hearing Casey’s opinions.

From there, I went down rabbit hole, which brought me to the junior resource companies and invariably, I heard Rick Rule speak.

Every time Rule speaks, there’s something to learn about what it takes to be a successful investor in the junior resource sector.

If you haven’t already, go to YouTube and search his name. Watch any of the videos and listen for the “how.†It’s in there and it’s invaluable.

Finally, and more recently, there is Jayant Bhandari.

Bhandari is a friend, a Libertarian, a fellow investor in the junior resource sector and a major influence in my life.

In a recent conversation, we covered a number of important topics about investing and life.

Bhandari’s insights will make you a better investor, of that I have no doubt.

Enjoy!

Brian: Current stock market dynamics can send investors on an emotional rollercoaster – seeing your portfolio plummet in value is something that most investors fear. Adding to this, there’s the risk that Covid-19 poses to you and your loved ones, which certainly has a compounding effect.

I have a two part question. First, with all the uncertainty in the market, do you view this as an opportunity to buy or is it time to sell?

Second, if it is an opportunity to buy, how are you able to put emotion to the side and take full advantage of the situation?

Jayant: I have been loading up. The best time to make money is in a bear market, when everything gets sold off, based not on valuation but on emotions.

When I buy something, I make sure to have a valuation. I always have a buy and a sell price for everything I own.

Even in a normal market, prices of individual companies are volatile. As I would have taken a calculated decision by trading in something, I do not beat myself up if thereafter the price changes against me, which almost always happens. Those who beat themselves up condition themselves to be emotional.

I want to restrain my emotions at all times. That way, I try to get objectivity to guide me. Of course, I make sure that I have enough cash at any point of time to not have to worry about my living expenses. If one has to worry about living expenses, one will inevitably get emotional.

One question remains. What is the best time to buy? How should one know when the proverbial knife has stopped falling?

I do not accept the concept of “falling knife.†There is no way to know when the market will stop falling. We cannot predict when it will turn around and start going up. So, when the price is right, I do what I intended to do. That, of course, means that I buy and sell too early. But those trying to perfect the timing keep waiting. For me, the right time is based on what I decided to be my buy and sell prices.

Brian: In my view, to be a consistently successful investor in the junior resource sector, you need to buy companies with good management teams that are selling at a price which is less than their intrinsic value, and have an acceptable risk profile.

In saying this, investors do have to be wary of value traps, which I define as companies that have the potential to never escape the market discount.

First, do you agree that value traps exist or is it just a matter of the investor getting the thesis wrong?

Secondly, if you do agree that value traps are out there, do you have any advice for steering clear of them?

Jayant: It took me a very long time to be respectful of the concept of “value-traps.†This concept is very hard to comprehend for anyone who makes objective judgements. A rational person thinks that, sooner or later, someone rational must start valuing a company based on its inherent value.

Most people like to think that the management of a company will take actions to correct the market perception or deploy capital in a way that the company gets the respect of the market.

Such an “objective†investor forgets to take into account the negative value that a bad management imposes on the company. “Value traps†are not just value traps, they are reflections of crooked or stupid management in command, who for whatever reason cannot be removed, and who impose a consistent negative contribution on the company.

An investor might erroneously think that stupid people cannot rise to the top. Alas, there are many ways to the top. My liking for the free-market does not fool me into thinking that it would be a panacea for all ills.

In general, I avoid any company run by a crooked or stupid management. Or at the very least, I account for the negative value that a bad management imposes on a company.

If you would like, I suggest you have a look at two companies, both that offer seemingly fabulous upsides, but are destined to stagnate.

One is G-Resources, a company that trades in Hong Kong (code: 1051). This company has a whopping US$1.5 billion in cash or cash equivalent. The company unfortunately trades at a mere US$0.23 billion market capitalization. There is seemingly a 550% upside. This looks unbelievable, but the problem is that making a hostile takeover of a cash-rich company does not work. The management gives no dividend and pays itself a very high salary. It is a no-brainer that despite seemingly such a huge upside, the cash will get frittered away, with an eventual value of likely zero.

Or look at Jubilee Exploration (JUB). This company has more in cash value than is its market capitalization. Based on my valuation, the company offers, perhaps, an easy 1,000% upside. Alas, a shareholder does not see how the upside will ever be paid out to him in dividend or capital gains.

Of course, both the companies I mentioned are not for people to buy, but to show how value-traps are real and why they might continue to exist to the end of the life of the company.

Brian: On March 23rd, the U.S. Federal Reserve, in an emergency FOMC statement, announced that they would essentially do everything in their power to prop up the American economy. They have dropped interest rates to 0% and have essentially indicated that they are prepared to infuse an infinite amount of money into the financial system.

The really crazy thing is that the Fed isn’t the only one taking these unprecedented steps. Countries around the world have pledged countless amounts of money to their corporations and citizens to minimize the impact of this global crisis.

In your opinion, will these financial measures be enough to contain the economic impact of the Covid-19 crisis and, if so, at what price has this containment come?

Jayant: Such “containment†measures are like an icing on the cake for an investor. When they were announced the stock market sky-rocketed. If I cannot fight it, I prefer to profit from it. I tend to buy more stocks when I know that they are falling because of lack of liquidity, for I know that the government would pitch in with more paper. Everything is immoral about this printing press.

From a macro perspective, however, printing money works as termite. It eats away the innards of any society, not just by destroying the capital by encouraging mal-investment, but also by imbuing immoral, irrational behaviour among the citizens. What becomes a personal relief for an individual is destructive to the society, which in the end is a mere transfer of money from one wallet to another, from the strong hands to the weak hands, along with massive loss of capital through friction (bureaucracy, regulations, etc.).

In any social emergency, there is indeed a need to keep the economy on ventilator to give it time to recover. However, when you must use the ventilator of the printing press, you pre-empt people within the society from helping each other, which is a more accountable system.

Fed’s printing press discourages people from saving during the good times, savings being what is needed to fight off the need to print money.

Brian: In my view, we live in

a society of paradigms or bias that lock us into thought patterns that keep

many of us blind to other alternatives that may be more efficient or

beneficial.

Whether it be financial, political or social, in your opinion, how does one keep an open mind and see through paradigms and their own inherent bias?

Jayant: Today the media and the institutional system encourages consumerism and hedonism, which are nothing but signs of decadence. My view is that the biggest reason we get set into a fallacious paradigm, which refuses to change despite evidence, is because of what have traditionally been know as sins. Our lust, greed and fear warp our thinking. We want to believe what suits our animal instincts. That does not mean that we necessarily supress our desires, but we must attempt to understand how they guide our thinking, conduct and decision-making.

Moreover, we are biological creatures and our habits and ways of thinking get encoded in us. It is very difficult for us to change our minds. My guess is that an awareness about this should make it easier for us to change when time comes.

Brian: In 2007, you wrote in an article entitled Twenty Observations of Liberty and Society, which was published in the Liberty Magazine,

“Every little bit of totalitarianism in our minds, however benign it may appear, helps to produce a complexly corrupt and coercive society, endlessly mirroring itself in the workings of the state. People should learn to see this connection. Libertarians should learn to see it. They should learn that the seedbed of oppression is not the state but the culture.†~ Liberty – pg.53

I think this is a very important insight, one that may not be completely understood by everyone upon reading it for the first time.

Can you please give us some context as to how you came to this realization and why it is important for people to learn to see it?

Jayant: I grew up in India, a grotesquely poor, wretched, superstitious, and backward society. I often meet Indians who are tired of corruption they face from the government. A moment later they happily offer bribes to get what they don’t have a right to, or they cheat their clients or customers. It is a society of distrust, where there is no moral code. Everyone is driven by expediency.

One corrupt bureaucrat I knew in Delhi told me once with tearful eyes how he had bought house for his son in London from the bribes he had collected. He then told me that his son was still expecting more and cheating him. What else did he expect when he had taught a certain moral code to his son?

Virtually every Indian I meet wants to be free, but desperately wants to control lives of other people.

Now, reflect of the above and tell me what kind of people will such a society supply to work in the government. What kind of motivations, drives and interests such bureaucrats have? What kind of incentive and feedback would such a society provide to those in the government?

Only in a society of moral and rational people can you expect a sensible government, which by definition will be minimal in size, and will constantly face forces for further reduction in its size.

Brian: Last year, you opened my eyes to the potential of East Asia, in particular, Singapore and Hong Kong. You have mentioned many times that, in your view, East Asia is the best hope for the future of humanity.

This statement has a lot of weight.

In your view, why is East Asia the best hope for humanity?

Jayant: Singapore, Taiwan, Japan, South Korea, and Hong Kong have not only kept a lot of their own values, of honor, respect, hard-work, loyalty, etc. but have strengthened them as a result of their interactions with the West. They have in a way adopted and adapted many of the good values of the western civilization, the one civilization I have know. The end product of this adoption is that East Asia today is more western in a good way that the West is today.

East Asia has not given much credence to the culturally Marxist forces that have emerged in the West over the last several decades, the forces that encourage hedonism, drugs, and a sense of entitlements and gradiences. This partly happened because East Asia is not necessarily democratic in the way that the West has become. So, the base desires of the masses do not reflect in the conduct of the government to the same extend. Moreover, East Asia has adamantly refused to accept refugees and immigrants, most of who come with a very strong psyche of expectations, and a sense of entitlement and grievances, which they readily impose on their hosts when they get the right to vote. Look at it this way, immigrants and refuges are carrier of the same cultural-virus they claim to be running from.

A homogenous society is, also, more trusting and loyal.

Of course, the leftist media of the West does not like East Asia and cherry picks bad aspects of it, corrupting western people’s understanding about East Asia. The fact that East Asia is not as democratic as the West is, it hasn’t brought in immigrants who refuse to assimilate, and hence retained many of the good qualities of the western civilization makes its goodness sustainable, when the West, alas, has started to sink.

I go to China several times a year. A lot can go wrong in China, but so far it has been on the same trajectory as South Korea or Japan was on at one point of time. Yes, there is tyranny, heavy-handedness and over-secrecy in China, but I am not comparing China with the US. I compare China from where it has arrived, a positive change unseen in human history.

My view is that the US does not have much time left. After Trump is gone, the US, given a massive demographic shift that is underway, will swing the US rapidly to far left. Without the crutches that the US is for the rest of the West, the West will start falling apart very quickly. The Third World stays relatively sober because of the fear of the US. That leaves only East Asia as the surviving sane part of the world.

But can countries like Japan defend themselves with the US presence? Again, while Japan might not call its armed forces as army, but they have a formidable defence force. East Asia will survive, or at least is the only area that has a hope of surviving.

Brian: On July 25th, in Vancouver, following the Sprott Natural Resource Symposium, you will be hosting the 2020 edition of the Capitalism & Morality Seminar.

In my opinion, Capitalism & Morality has no comparison; its structure and list of speakers are unique and of the highest quality. I wouldn’t miss it and am honoured to be a part of it this year.

Past speakers include Rick Rule, Doug Casey, Adrian Day, Albert Lu, Stefan Molyneux, Frank Holmes, Butler Shaffer, Keith Weiner and, of course, yourself.

The first Capitalism & Morality Seminar was in 2010 and has grown dramatically over the last 10 years.

Looking back to the seminar’s beginnings, what was your motivation to host such an event and what can people expect from the 2020 edition?

Jayant: I immigrated to Canada for one reason. I was searching for liberty and wanted to live in western civilization, which, I must restate, is the only civilization. Even East Asia is a civilization today because they have adopted the western ways of life and thinking. In running Capitalism &Morality, I want to, in my very little way, contribute towards protecting the greatness of western civilization, which is what distinguished humanity from animals.

The seminar has grown in support every year. And I am excited that you will be anchoring a panel discussion this. All I can say about this year’s seminar is that it will be better than the earlier ones.

Your subscribers can get 10% off the price for the seminar by using coupon code, LENI. Anyone who pays, attends the whole day, and thinks he did not get value for money can ask for a full refund. Also, those who want to watch from home can do so for free on YouTube.

Get the e-book Junior Resource Sector Investing Success: The Risks, Rules & Strategies You Need to Know today, when you become a FREE Junior Stock Review VIP .

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review Premium

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria