Does successful investing within the junior resource sector start with choosing the right metal?

I’ve said it many times, I believe speculating in the direction of a metal price is essentially impossible to do with any consistency, and shouldn’t be the reason for investing in a junior resource company.

This statement is more controversial than I had imagined and has been challenged many times over the last 3 or 4 months.

Let’s use the gold price as an example. The narrative surrounding higher gold prices can take many forms, but for most people, a higher future gold price is driven by the instability of the global financial system, which has been propped up by quantitative easing and low interest rates throughout the world.

I have no issue with that argument.

However, from 2011 to 2015, the gold price was almost cut in half and, as we all know as junior resource sector investors, besides the 8 month blip in 2016, the juniors, on a whole, have been in a bear market since 2012.

So why the precipitous fall from grace?

- Must have been the miraculous repair of the global financial system.

Not a chance. In my opinion, the global financial system has only worsened over the last 8 years. Countries are more in debt than ever and interest rates continue to be near record lows.

- So, it must be gold supply manipulation by the world’s central banks.

Maybe, but honestly, I find it very hard to accept any thesis on gold supply and demand considering that, essentially, all the gold ever mined still exists.

- US$1900/oz was too high, the market over valued the amount of risk in the global market.

I’m not sure I have heard anyone use that argument to explain the fall in the gold price, but I think that there is some sensibility to it. Personally, though, given where we are today, I think we will see the gold price break US$2000/oz.

When? Great question! I have no idea and there-in lies one of the main issues with metal price speculation.

In reality, given a long enough timeframe, you can be right about the direction of the metal price, however, given the time value of money, are you actually right?

My point with this example is to show that while the popular narrative and the fundamentals of a metal appear to be pointing to a rising metal price, global markets are complex and hard to predict.

Thus, it’s my opinion that especially for the average investor, there’s very little value in trying to guess or follow someone who believes that they can predict the direction of a metal price.

If you’re bullish on the metal, buy the metal – it doesn’t come with the risk associated with the miners, who can lose you money due to a variety of factors that include exploration failure, poor metallurgy or political strife.

Successful investing in junior resource companies is predicated on 3 main criteria: Invest in the best people, protect your downside risk, and be a deep thinker – see through the popular narrative.

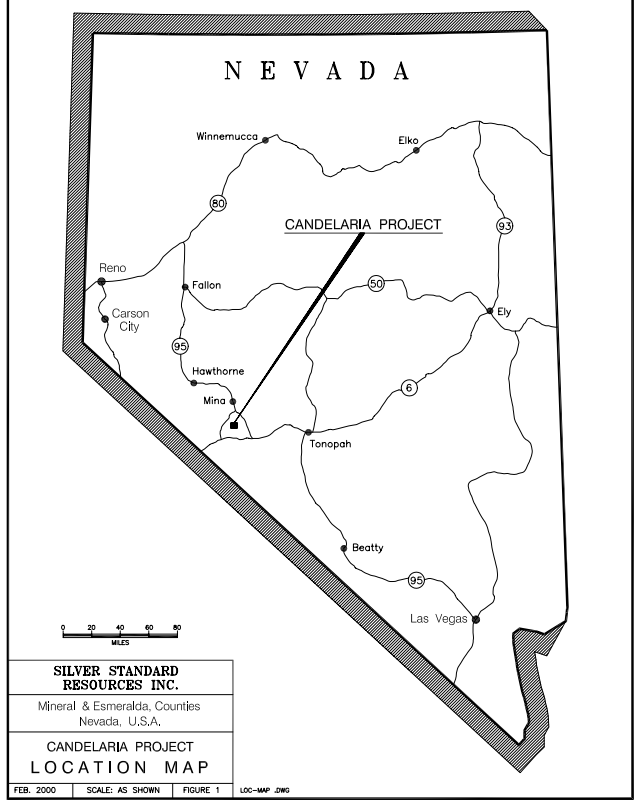

Today, I have for you the details from Day 1 of my Nevada Site Visit Tour, where I had the chance to visit Silver One Resource’s flagship Candelaria Project, which is located in the northwestern portion of Nevada, near Hawthorne.

Let’s take a closer look.

Reno, Nevada

On October 28,th I caught the 6:20am flight out of Toronto to Denver and hopped on a connecting flight which brought me to Reno, Nevada before noon Pacific time.

Unless you’re travelling to Las Vegas, in my experience, Nevada is always multiple flights from the east coast. It’s even worse if you’re flying into Elko, Nevada, which is located in the northeastern portion of the state – it’s been a marathon 3 flights the last 3 times I’ve taken the trip.

Flights aside, I really enjoy this part of the United States. The air is fresh and clear and once you leave the cities and begin to travel into the smaller towns, it’s like going back in time from a number of perspectives.

After landing in Reno, we made the 3ish hour drive south to Hawthorne, where we spent the night. The next morning, it was a short drive to Candelaria and a good review of what Silver One is planning at its flagship asset.

Source: Technical Report

Hawthorne sits directly south of Walker Lake and, interestingly, is home to the world’s largest ammunition depot. The depot covers 147,000 acres and has over 600,000 square feet of storage space within 2,427 bunkers.

Unfortunately, I don’t have a picture to share. You will have to trust me when I say that it’s an amazing sight to see and really confusing if you don’t know what you’re looking at.

Besides being home to the world’s largest ammo depot, Hawthorne is home to 3,000 people.

At our hotel, at least half of the guests looked to be with the mining industry in some shape or form. The other half were older couples, whom I’m sure were using Hawthorne’s Travel Lodge as a stopover on their way to Las Vegas.

Silver One Resources (SVE:TSXV)

MCAP – $44.79 million (at the time of writing)

Shares – 149.3 million

FD – 187.1 million

Strategic Shareholders – Eric Sprott 10.8%, SSR Mining 6%, Insiders 5.5%, First Mining Gold 3.4%

NOTE: Silver One closed a $4.976 million financing at a share price of $0.125 and a 3 year – ½ warrant at $0.20 on July 11, 2019. The PP shares will be free trading very soon and there’s a chance that some buyers may sell their shares and hold the warrants moving forward – FYI.

Candelaria Project

NOTE: Silver One has 1 remaining $1 million option payment on Candelaria, which is due in January 2020 to Silver Standard. Additionally, under the option agreement, Silver One must assume a $2 million reclamation bond relating to the historic heap leach pads at Candelaria. Instead of coinciding with the last option payment, this will be deferred until January 2023.

Being a past producing mine site, the Candelaria project has great infrastructure. It begins with close proximity to the interstate and a paved road right up to the main gates of the project.

Turning off the interstate, power lines follow you up and into Candelaria, with the sub-station sitting right next to a steel building. This is where Silver One is currently holding samples and other exploration equipment.

Additionally, Candelaria has access to water via wells that produce 500 to 600 gpm, I’m told, and sit in the southern portion of the property.

NOTE: From 1980 to 1999, the Candelaria mine produced 47 million ounces of silver before being closed due to low silver prices.

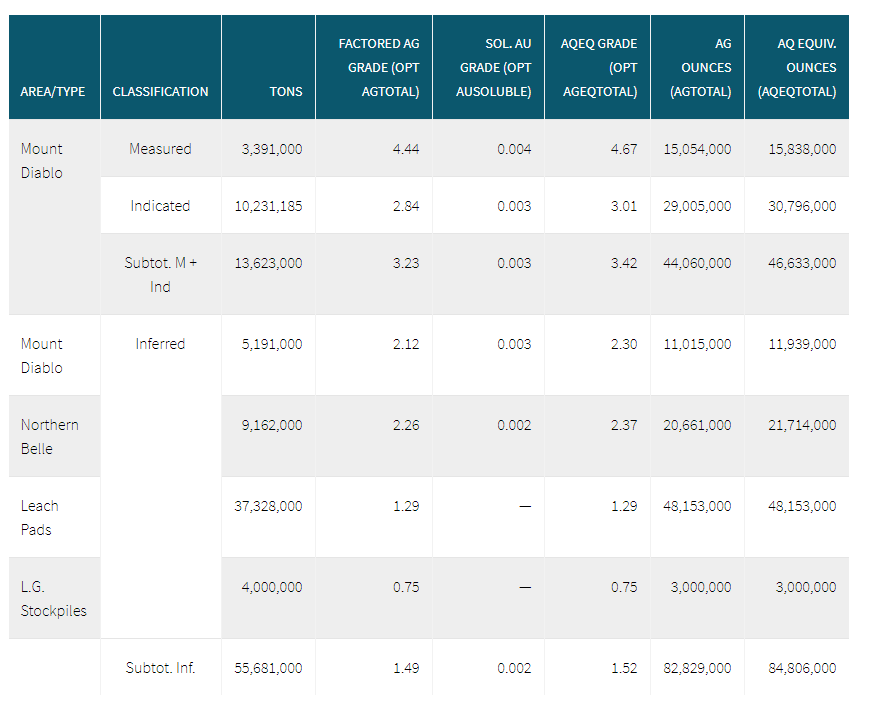

Historical Resource

The Candelaria project has no 43-101 compliant resources on any of its heap leach pads or deposits – Northern Belle, Mount Diablo, Lucky Hill Mine or Georgine Pit.

Thus, the historical resource table which I have included for your reference should be taken with a grain of salt.

HISTORICAL RESOURCE – NOT 43-101 Compliant

Silver One’s CEO, Greg Crowe, who led much of the discussion during the site visit, mentioned that an updated resource was a priority for the company moving forward.

In fact, most of the drilling this fall will be used to produce a 43-101 compliant resource.

Metallurgy

In terms of priorities, next to setting a base number for Candelaria’s resource estimate, the company will also focus a lot of attention on the project’s metallurgy.

As it stands right now, roughly 30% of Candelaria’s silver is non-recoverable through coarse grinding and cyanide leaching.

Preliminary mineralogical testing suggests that most of this non-recoverable silver is held within jarosite.

Having 30% of your resource non -recoverable is significant and, thus, is why it’s a priority for Silver One to improve.

NOTE: Initial metallurgical results show that 56% of the silver on the heap leach pads is cyanide soluble, leaving 44% in the non-recoverable category.

In my view, the metallurgical work represents biggest opportunity for the company. How or where else can they add that many payable ounces within a year for what is a fraction of the cost and risk of drilling.

Crowe explained that they are focused on finding the optimal milling (grinding) size needed to liberate the silver from the jarosite.

Of course, the amount of milling has to be balanced with the economics of the whole process. It’s one thing to liberate all the silver out of the jarosite, but if you need $50 silver to do it, is it worth it?

It will be very interesting to watch for these results, and much like the resource estimate, see what silver price is needed for this to be economic.

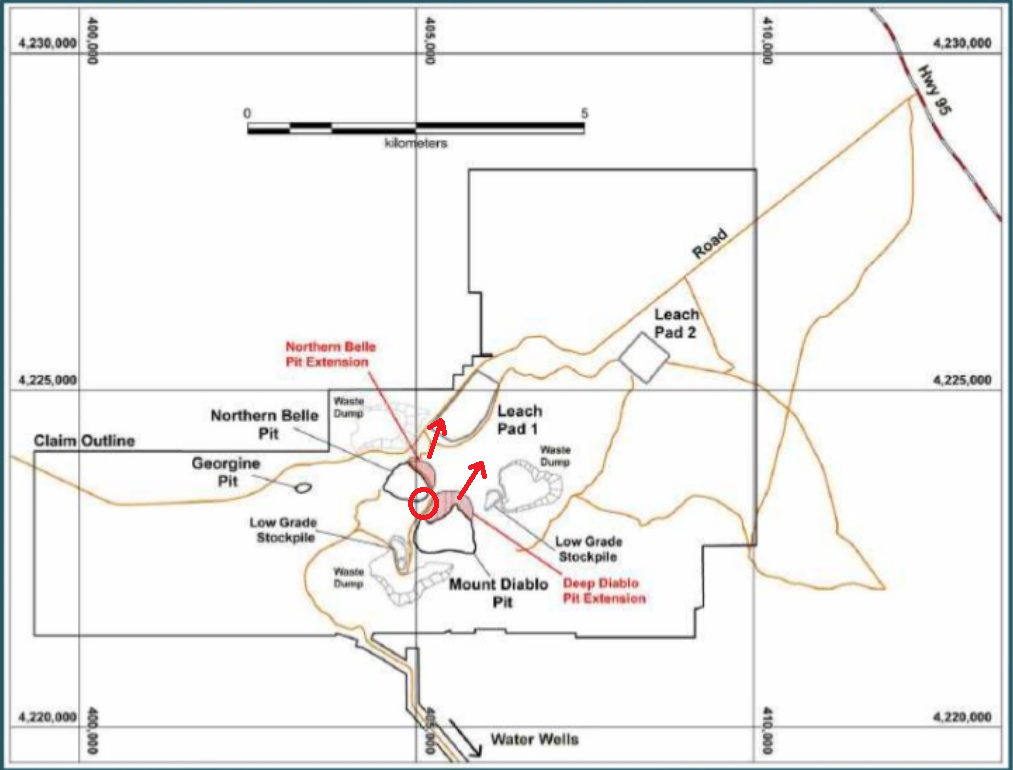

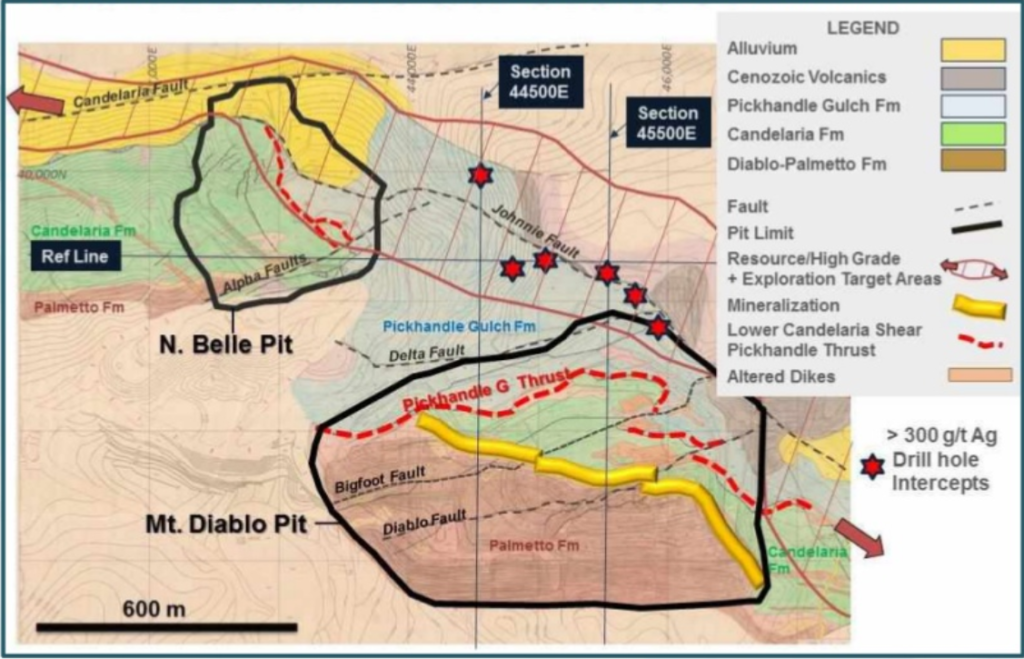

Drill Targets

Next to the Candelaria’s priority work, the resource estimate and metallurgical testing, there are some interesting exploration drill targets across the entire property.

I will draw your attention to the image above, which gives us a top view of the project.

The Northern Belle and Mount Diablo pits are labelled and sit on either side of the red circle.

The first 2 targets are the most obvious. Silver One will be drill for down dip extensions, which I have represented using red arrows, on both pits.

Second, both deposits will be drilled for lateral extensions, specifically in between the 2 pits to see if they connect. Represented as the area within the red circle.

Historic Silver Standard Drilling

Historically, Silver Standard did hit silver mineralization in a number of holes in between the 2 pits, represented as stars in the image above.

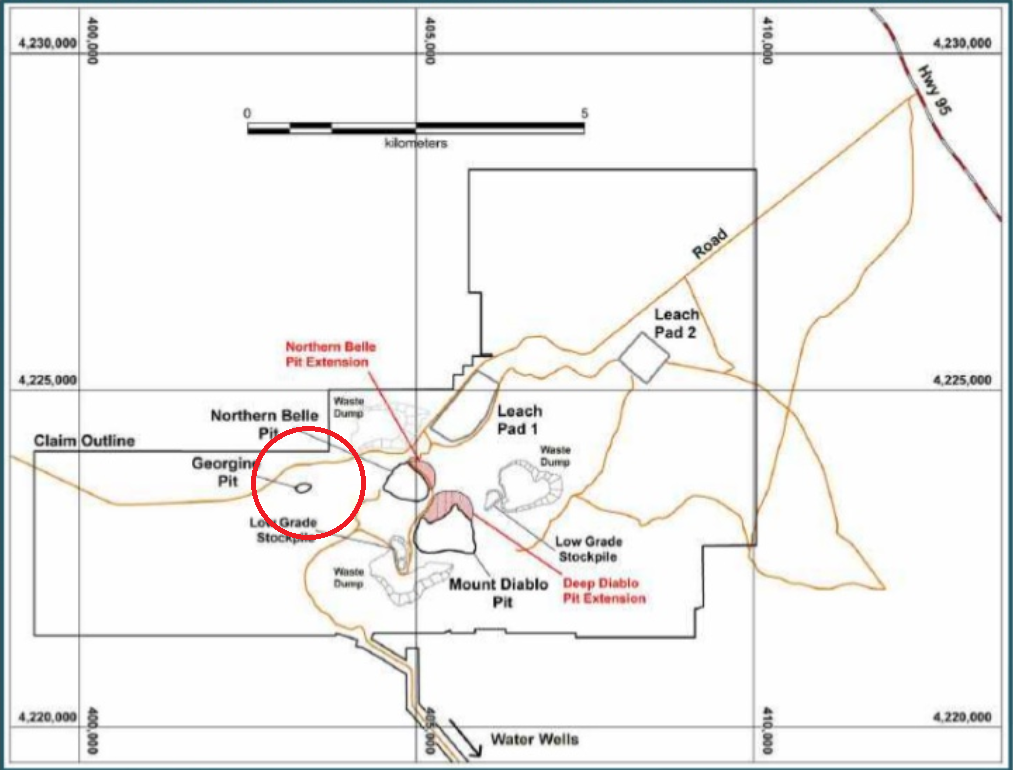

Georgine Pit

Now let’s take a look at the more abstract exploration targets at Candelaria.

In the image above, I have circled the next most prospective area within Candelaria.

This region of the property is interesting as it either represents a parallel or off-set mineralized structure to that which hosts Northern Belle and Diablo.

Currently, there are 2 known past producing pits in this area – Georgine and the Lucky Mine. Both are small, but when mixed with the magnetic anomaly the company has identified, could represent a much bigger system.

I couldn’t find a picture, but Crowe mentioned that the magnetic anomaly lies just north of the Georgine pit. Given this, they subsequently staked more ground along the north claim boundary you see in the image above. The new claim block represents an area of approximately 8 square kilometres.

Another interesting note on this area is the grab samples they have found. Crowe showed us one of the high grade copper, low grade gold samples they found in the immediate area surrounding Georgine.

Sample found near Georgine Pit

Crowe speculated about the possibility of there being an Iron Oxide Copper Gold (IOCG) deposit in this area.

They plan to follow up the grab sample with an IP survey, which could shed some light on any concentrations of sulphide mineralization in the area.

Concluding Remarks

It was a good site visit to Silver One’s Candelaria project, I believe I have a good understanding of where the company is and where they are headed.

I look forward to seeing the initial drill results from the company, which I am sure we will see before the end of the year. Additionally, more geophysical work on the new claim block and area surrounding Georgine pit should be really revealing to what may be there.

I, however, am not a buyer of Silver One Resources at this point; as there are a number of questions I have yet to answer.

First, will there be an onslaught of selling as this summer’s private placement shares become free trading?

Second, the metallurgical work is a HUGE part of this story and, really, I think, will be the main factor in classifying it as a good or great project.

Silver One has been added to my watchlist, as I eagerly await drill and preliminary met work results.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with any of the companies discussed in this article, however, Silver One Resources did pay for my site visit expenses. I do NOT own shares in Silver One Resources.