Continue reading Cornish Metals – A Conversation with CEO Richard Williams

NOTE: This article was originally published for Junior Stock Review Premium readers on July 3rd, 2020. Subsequently, Monarch’s share price has appreciated 20%. Get my best investment ideas first by becoming a member today.

Finding companies that are trading for less than their value is integral for success in the junior resource sector.

With that said, investors have to be cognizant of why the company is trading at a discount to its value.

Value traps do exist and can either put your investment dollars into neutral or worse – lose you money.

You must, therefore, spend the time to understand the reasons for the discount and decide if it’s realistic, given the company’s action plan, to change the market’s perception.

In my research to identify the top M&A candidates in the sector, I have found that the companies that fall in this category are well known in the market and, in some cases, trade at a premium to their value.

The company I have for you today is not only trading at a steep discount to its value, but it also has, in my opinion, all the makings of a premier M&A candidate.

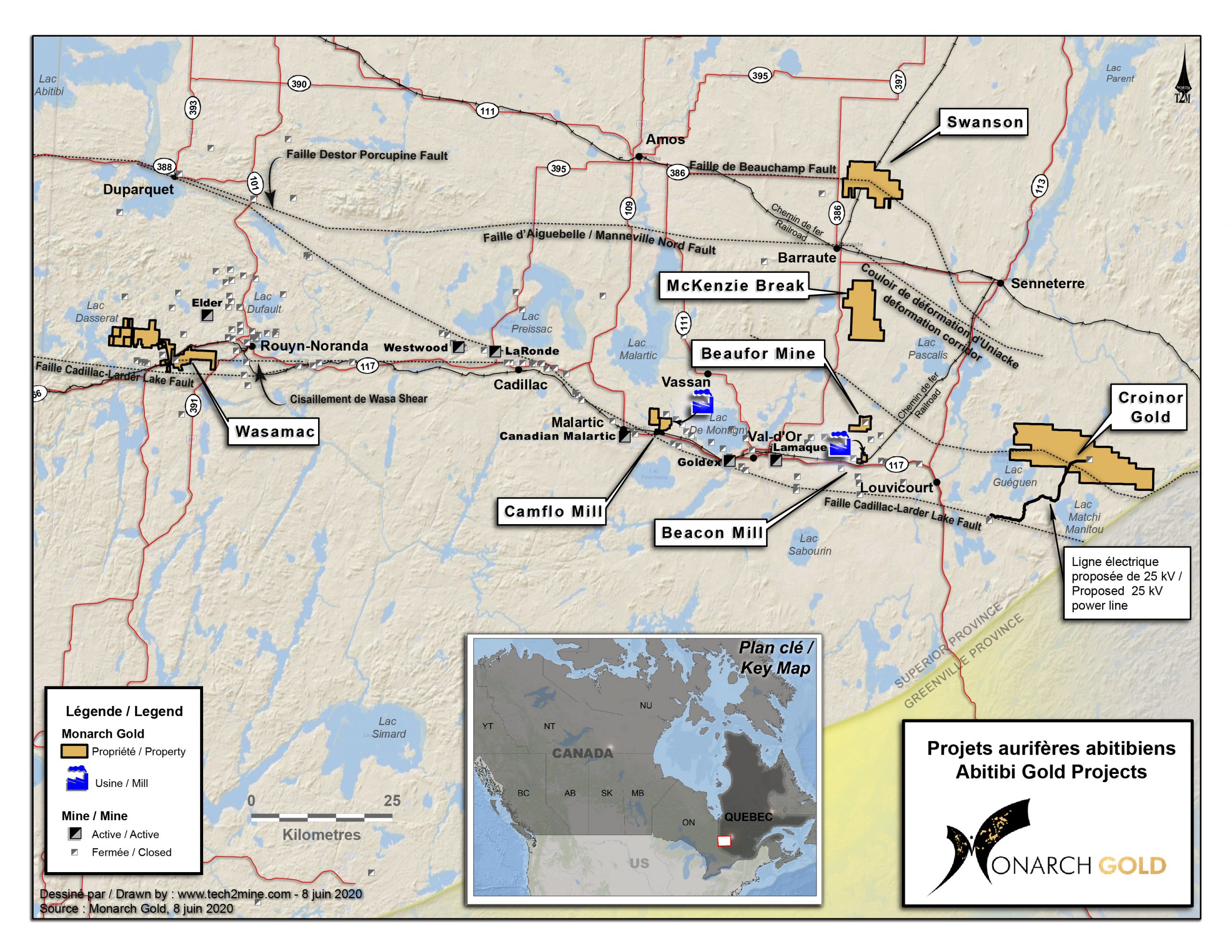

The company is Monarch Gold and they are developing their flagship Wasamac project in the heart of the world-famous Abitibi Greenstone Belt.

Let’s take a closer look.

MCAP – $141.6M (at the time of writing)

Shares – 294.1M

FD – 333.7M

Cash – roughly $25M

Strategic Investors – Alamos Gold (16%), Yamana Gold (6%), Hecla (4%), Agnico Eagle (3%)

Total Equity Holdings –$3.2M As of March 31st, 2020 (O3 Shares, Probe Metals, etc.)

Debt – $3.8M of which $2.4M is due this year.

Monarch Gold is led by CEO Jean-Marc Lacoste. Lacoste has a financial background and, in my opinion, a clear understanding of how to add value to a junior resource company.

Over his close to 8 years as CEO of Monarch, Lacoste has demonstrated that he and his team are able to execute the company’s vision of acquisition and development.

The ability to buy projects cheaply, add value through exploration and development, and then have the wherewithal to make a deal and sell the project to unlock the value for shareholders isn’t done successfully, all that easily, in the junior resource market.

Lacoste and supporting cast are clearly capable of executing this process and, given the current market, should be able to reap the benefits of multiple years of practice.

Lacoste is supported by CFO Alain Levesque, VP Corp Development Mathieu Seguin and VP Operations Marc-Andre Lavergne, together with a committed board of directors which has a strong track record of mine discovery and development.

I’m confident that the Monarch Gold team has the experience and focus to unlock the value at Wasamac and the rest of their secondary projects.

As I mentioned in my intro, I believe Monarch is trading at a discount to their value.

As investors, we must try and understand why.

In Monarch’s case, at least a portion of the issue, I think, is directly related to the upfront capital cost and low after-tax internal rate of return (IRR) reported in Wasamac’s 2018 FS.

Wasamac 2018 FS Highlights:

At US$1300/oz gold

When you examine the numbers, you can see that the upfront CAPEX and the IRR stand out like a sore thumb.

Let’s start with the upfront CAPEX, which is estimated at $464M, and includes roughly $230M for the mill and tailings facility.

This is a good chunk of cash, especially when put into context with other gold projects of similar size – it is much higher.

A big reason for this, at the moment, is that most of Wasamac’s comparisons are open-pit mines, which do typically have lower upfront capital costs – but not always.

Second is the poor after-tax IRR of 18.75% at US$1300/oz gold.

For those who are not aware, IRR is a measure of profitability, comparing the upfront capital cost to the estimated cash flow.

For further perspective, the best gold projects typically have after-tax IRRs over 25%.

Now, at today’s gold prices, Wasamac’s after-tax NPV and IRR increase and, most importantly, bring the IRR above the 30% mark – which is great.

Wasamac’s comparables, however, also respond well to rising gold prices and, therefore, are still better.

In my view, the stigma of these metrics has resulted in the discount to value, thus far.

The obvious question is, then, how does Monarch improve the upfront CAPEX cost and IRR metrics?

On May 14th, Monarch announced a MOU with Glencore regarding the potential use of the Kidd concentrator in Timmins, Ontario for the treatment of ore to be mined from Wasamac.

The MOU consists of 4 stages: Phase 1 – Upgrading Study (to be completed before Dec.31, 2020), Phase 2 – Negotiation and Signing of a Toll Milling Agreement (to be completed before March 30, 2021), Phase 3 – Concentrator Upgrading Work (to be completed before July 31st, 2021) and, finally, Phase 4 – Performance of the Toll Milling Services (First delivery to take place by Dec.31, 2023).

Further, on June 22nd, Monarch awarded the Phase 1 Upgrading Study on the Kidd Concentrator to Ausenco Engineering Canada.

These steps, if executed and with acceptable results, have the ability to address the 2 issues which I think have been impacting Monarch’s valuation, and could result in a substantially higher IRR.

To add, I believe the addition of Yamana (YRI:TSX) to the list of Monarch’s strategic investors is a bigger deal than the market has given it credit.

Yamana not only participated in the latest financing, but also wanted a Board of Directors seat, which I think is very telling with regards to future possibilities.

Clearly, to me, this move suggests that Yamana sees the potential in Wasamac.

With the Canadian Malartic mine, their 50% owned operation, sitting just east of Wasamac, it’s possible that Monarch will have another option outside of Glencore’s Kidd Concentrator when it comes time to negotiate terms of a toll mining scenario.

Plus, it’s entirely possible that a deal with Glencore, and Monarch’s valuation at the moment, could push Yamana to acquire Monarch.

That is entirely speculation, but something that, I think, has weight.

Either way, Wasamac’s resource size, production profile, sensitivity to higher gold prices and location put it at or near the top of my list of M&A targets.

There is far more to the Monarch Gold story than just Wasamac, with 4 other advanced stage projects in the Beaufor Mine, Croinor Gold, McKenzie Break and Swanson projects.

Additionally, Monarch has 2 fully permitted mills in Camflo and Beacon.

Clearly, project development in the Val d’Or region of the Abitibi is a major part of Monarch’s growth strategy.

Further, scanning their news releases, you will find a history of acquisitions and sales.

A great example of this comes from earlier this year with the sale of Monarch’s Fayolle project to IAMGOLD (IMG:TSX) for $11.5M.

A willingness to monetize secondary projects for cash and/or shares is a great way for Monarch to advance their flagship Wasamac project without further dilution to existing shareholders.

As Lacoste mentioned to me in conversation, the focus is Wasamac and Monarch becoming a +100Koz/year producer.

The proceeds and the reason for the investment and development of these secondary assets is to, therefore, progress Wasamac with as little dilution to shareholders.

Let’s take a closer look at their current project inventory and the potential value that it could unlock for the company moving forward.

Let’s begin with the 2 mills – Camflo and Beacon.

Camflo Mill

Beacon Mill

So what are they worth?

That’s a great question and one that is hard to answer.

For perspective, along with at least a 5-year development and permitting timeline, the upfront capital needed to construct a new mill could be in the order of $40M to $50M.

With that said, we do have a recent deal on a mill in the Val d’Or area which I think we can use as a conservative estimate for the value of Beacon and Camflo.

In May, O3 Mining (OIII:TSXV) acquired QMX’s (QMX:TSXV) Aubrel Mill for $5M.

With that set as our precedent, we will assume Camflo and Beacon are worth $5M each.

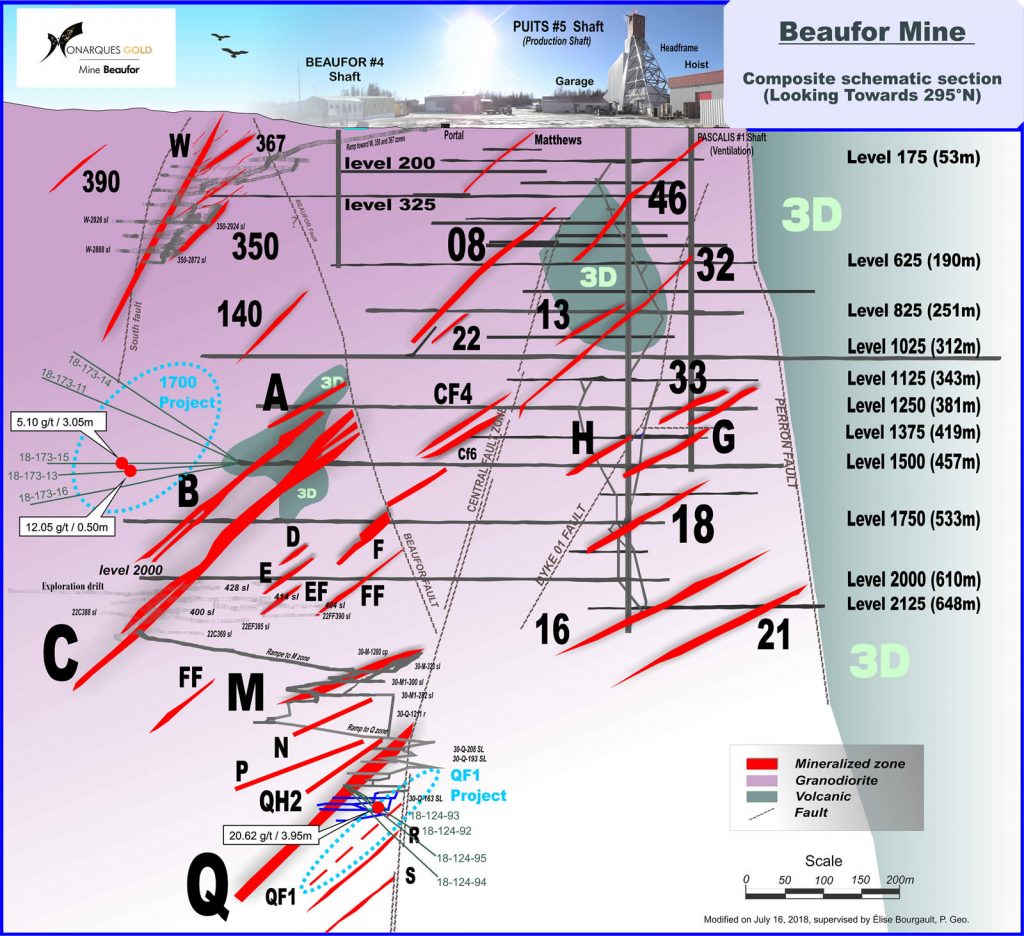

Next to Wasamac, the Beaufor Mine is arguably Monarch’s 2nd most important asset, as it was a producing mine up until last summer when it was put on care and maintenance.

Beaufor was formerly owned by Richmont Mines, who sold it to Monarch along with the rest of its Quebec assets before being acquired by Alamos Gold in 2017.

Beaufor presents an interesting dynamic to Monarch’s valuation, because it both proves the management team’s ability to operate a mine and gives the added potential for cash flow moving forward.

On May 7th, Monarch announced that they had sold a 3% NSR on the Beaufor Mine to Caisse de depot et placement du Quebec (CDPQ) for $5M (with the option to redeem up to 2%).

This cash will be put to work right away with a 42,500m drill program, which currently has 95 high grade gold targets, many of which are below 800m.

Monarch has retained the services of Goldspot Discoveries (SPOT:TSXV), which uses their expertise in geosciences and advanced artificial intelligence algorithms to aid in the efficiency and success rate of exploration.

The company hopes to delineate enough resources for 3 to 4 years of production and are targeting a re-start of the operation by Q1 2021.

So, economically speaking, what can we expect from Beaufor upon re-start?

That’s a very important question.

As I mentioned, last summer, Beaufor was put on care and maintenance because it was losing money at roughly US$1350/oz gold.

We can conservatively say, therefore, that the operating cost moving forward is probably around US$1400/oz gold.

At gold’s current price, therefore, we are looking at a profit margin in the order of $300/oz, which is great.

Monarch operated Beaufor for 18 months prior to shutdown and was producing at a rate of roughly 20,000 oz per year.

Now, assuming that this is the rate which they will produce at in the future, we can make a rough estimate that Beaufor could cash flow $6M a year.

Honestly, though, considering that the company is targeting grades much higher than the 4.5g/t gold, which they were mining prior to the shutdown, the cash flow generation could be much higher.

For the sake of this valuation, let’s assume that Beaufor on a discounted basis is worth $20M.

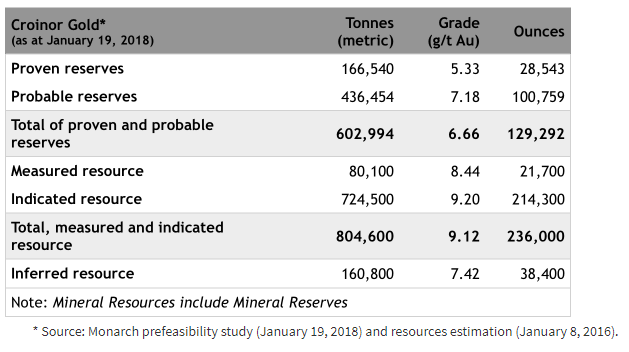

The Croinor Gold project sits just 55km east of Val d’Or and encompasses over 151 square kilometres.

Croinor is well developed with a 2018 PFS on the project.

Croinor Gold Project 2018 PFS Highlights:

At US$1280/oz gold

Using the PFS sensitivity table, you can see that at roughly today’s gold price, US$1664/oz, the after-tax NPV of the project increases to $50.64M.

Now, these aren’t earth-shattering numbers, but I can clearly see how Croinor has the potential to be a great spin out or acquisition target for a new junior gold company – especially given the current market dynamics.

For the sake of our valuation, let’s assign a value of $15M, which is roughly 30% of the project value given the current gold price.

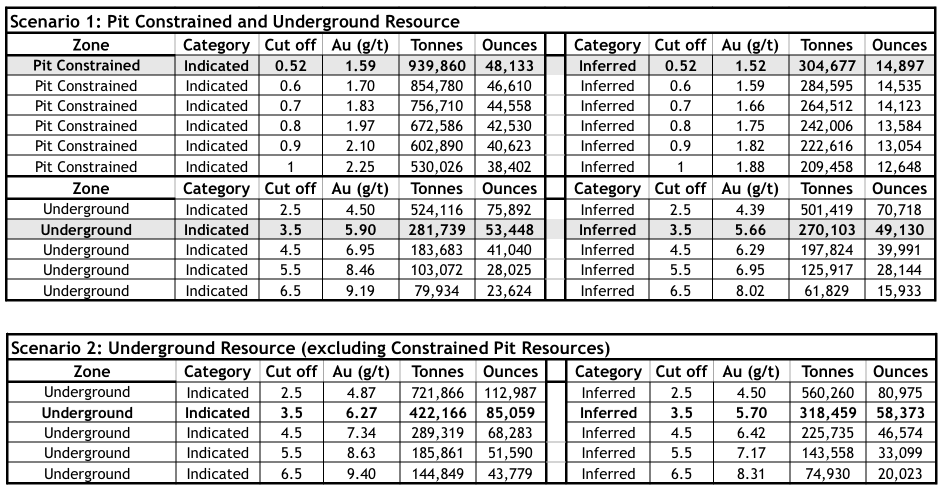

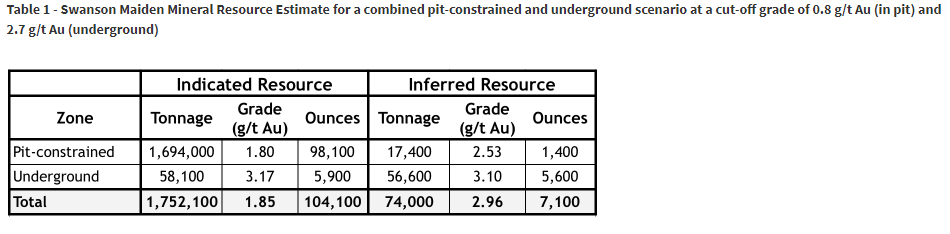

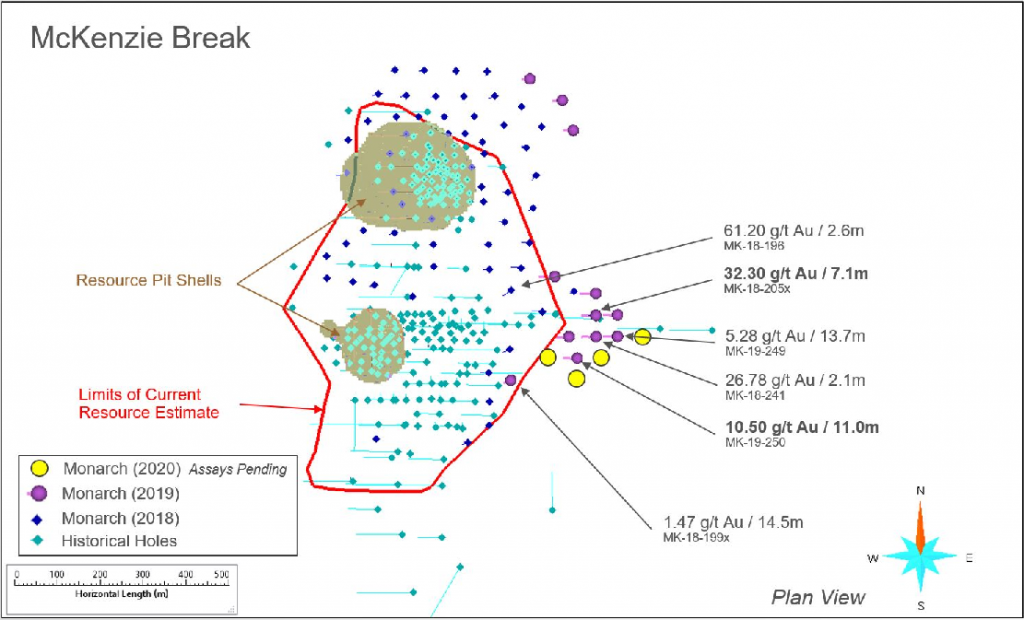

Last but not least, we have the McKenzie Break and Swanson projects.

Both projects have 43-101 resources, but no economic studies completed on them.

Most notably, exploration drilling below the current resource at McKenzie Break returned some fantastic intervals in February which were highlighted by:

Monarch plans to follow up and continue to explore the McKenzie Break property. It recently completed a 1,600-metre drilling program, with results pending.

Building on these results will further increase the value of the project and make it another prime candidate for Monarch to sell into this high gold price environment.

To round out the valuation of Monarch’s secondary projects, let’s assume that collectively the McKenzie Break and Swanson projects are worth $5M.

Gold Price – The gold price remains, in my opinion, the biggest risk to Monarch Gold’s share price. As I have noted before, however, this risk is ubiquitous across the sector. In my view, the gold thesis has never looked better and, thus, I’m inclined to think that there is a much better chance we will see higher gold prices ahead – time will tell.

Covid-19 – The Covid-19 pandemic continues to present a risk to the entire world. For companies such as Monarch, the risk is in the delayed development of their projects. A 2nd wave of lockdowns due to Covid-19 could put Monarch’s action plan on hold and, therefore, provide little return to investors as cash would only be going to G&A.

At this point, it’s still hard to say where we are headed this fall.

Wasamac – It’s entirely possible that the market will not recognize the value of Wasamac until there is more clarity on the reduction in upfront CAPEX costs. Ausenco is mandated to have their report completed by October of this year, so we should have a good idea of the cost of upgrading the Kidd concentrator by then.

In my estimation, I’m guessing we will see a number of around $50M. Therefore, the overall savings with the toll milling agreement should be around $180Mish.

Will this be good enough for the market?

Remember, the Wasamac gold project is one of only a handful of projects in Canada and the United States that has had an FS completed and has the production capacity of at least 100Koz/year.

With that in mind, I think it’s only a matter of time before the market recognizes Monarch’s true value.

Putting it all together, Monarch has roughly $25M in cash, a total equity holding of $3.2M (this is most likely higher given the market dynamics), and, conservatively, has a collection of secondary projects that are collectively worth $50M.

The market is, therefore, currently valuing Wasamac, which is a FS level project with an after-tax NPV@5% of $750M at the current gold prices, at approximately $63.4M.

In comparison to its peers, no matter how you slice it, this is incredibly cheap.

With that said, Monarch does have some work to do to improve on upfront CAPEX costs for Wasamac.

They must make a good deal with Glencore or another suitor in the area to toll mill Wasamac’s future production.

The economics of the toll milling agreement will be officially shown in the updated FS, which is expected next year.

Along with this, they must continue to development and have an eye to monetize the secondary projects within their portfolio.

Given the current market dynamics and very strong case for high gold prices, Monarch is in an enviable position when it comes to negotiating for the best deals on their projects.

Monarch Gold is selling at a fraction of its value and, given management’s plan for the next 6 to 12 months, I believe it’s only a matter of time before their value is recognized.

I am a buyer of Monarch Gold (MQR:TSX).

Get the e-book Junior Resource Sector Investing Success: The Risks, Rules & Strategies You Need to Know today, when you become a FREE Junior Stock Review VIP

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review Premium

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with Monarch Gold Corp (MQR:TSX). I do own shares in Monarch Gold Corp.

NOTE: This article was originally published on June 23rd, 2020 for subscribers. Subsequently, the share price has risen 40%.

As I mentioned in last week’s Market Update commentary, M&A is on my mind.

This new bull cycle in gold will bring fourth many new deals and with them a chance for investors to make a very good profit – if you choose right.

Picking the right company will be a reflection of the criteria you use.

Being picky and setting the bar high not only protects your downside risk, but also forces you to think like a major mining company, which is looking to add economic resources to their books.

Today, I have for you one company which I believe will be at the forefront of M&A activity in the not-so-distant future.

The company is Integra Resources (ITR:TSXV) and they are developing their flagship Delamar project in Idaho.

Let’s take a closer look.

MCAP – $190.1M (at the time of writing)

Shares – 119.6M

FD – 130.7M

Cash – roughly $27M

Integra is led by CEO George Salamis, who has over 30 years experience in the resource sector and is a geologist by trade.

Salamis has a very good reputation in the sector and the resume to support it.

He has been involved in over $2B inM&A transactions over his career, with his most recent success coming from the acquisition of Integra Gold by Eldorado Gold Corporation for C$590M.

Salamis is supported by a strong team with CFO Andree St-Germain, VP Exploration Max Baker, and COO Tim Arnold.

Further, Integra has a great Board of Directors; Chairman Steve de Jong, David Awram (Co-Founder of Sandstorm Gold), Timo Jauristo (Former Executive VP with Goldcorp), Anna Ladd-Kruger, and C.L. “Butch†Otter.

Finally, and although not a Director, Strategic Advisor Randall Oliphant (Former CEO of Barrick Gold) brings 30 years of experience to the table.

Clearly, Salamis and his supporting cast have a history of developing projects into premier M&A candidates.

I fully expect to see the same story play out with Delamar, as the team works to improve Delamar’s economics and this gold bull market progresses.

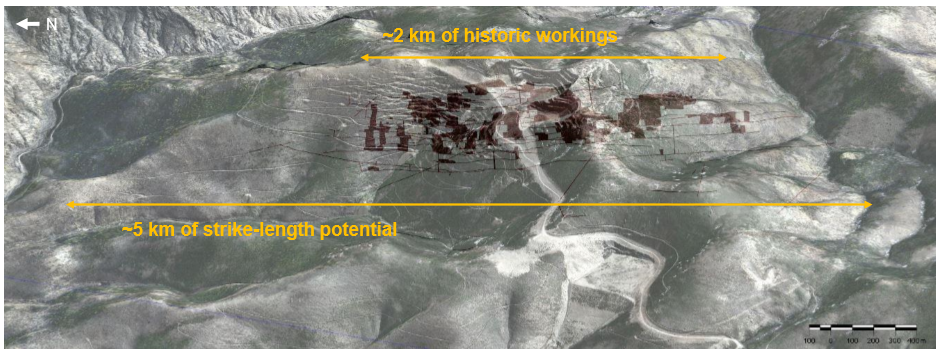

The Delamar project encompasses roughly 8,100 hectares in southwestern Idaho, about 80 km southwest of Boise.

Idaho is a premier mining jurisdiction and, while it may not have as deep a history and fanfare as its neighbour to the south, Nevada, it does rank very high in mining investment attractiveness.

In fact, the Fraser Institute agrees and ranks Idaho 8th in the world in mining investment attractiveness with a score of 82.78.

Delamar is a past producing mine and, prior to its acquisition by Integra in 2017, it was owned by Kinross.

The Delamar and Florida Mountain deposits have produced an estimated 1.3 million ounces of gold and 70 million ounces of silver over the course of their 100 year history.

Since its acquisition, Integra has converted 90% of its inferred resources to M&I between 2018 and2019, it has completed extensive metallurgical studies on both the oxide and sulfide portions of the deposits, and completed a PEA last fall.

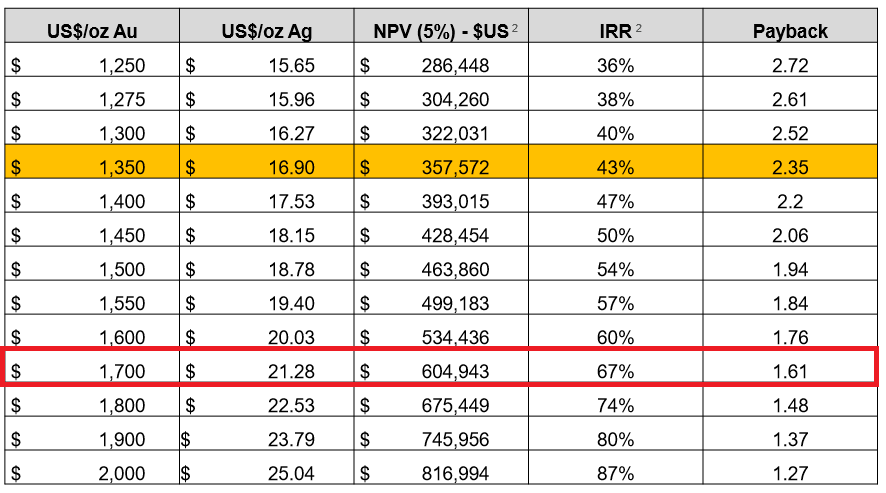

The PEA reveals robust economics at US$1350/oz gold and US$16.90 silver. Let’s take a look at some of the highlights.

2019 Delamar PEA Highlights:

After-tax NPV@5% – C$472M

After-tax IRR – 43%

Upfront CAPEX – US$161.0M

Sustaining CAPEX – US$93.4M

AISC – US$742/oz AuEq

Production Capacity – 124 Koz/year AuEq

Life of Mine – 10 years

M&I Resources – 1.8 Moz AuEq

These are great numbers, as the project has good size, comparatively low upfront capital costs, and the gold and silver price assumptions are well under today’s prices.

How does the project’s economics look at today’s metal prices?

Great question; while it’s imperative to understand our downside risk in-terms of the metal prices, we need to understand the value of the project today.

In Integra’s corporate presentation, there’s a great sensitivity table which reflects Delamar’s NPV and IRR and varying metal prices.

Highlighted in red is a snap shot of today’s metal prices. I will note that the silver price isn’t anywhere near US$21.28, yet, but silver’s impact on the project is much lower than gold’s given the metallurgical recoveries at this point.

The other thing to consider is that this sensitivity analysis only changes the metal price, it doesn’t account for the other positives that are derived from higher gold and silver prices.

Most notably in this base case scenario, is the increase in the pit shell and the possibility of mining underground, which is a very good possibility given the mineralization which Integra has encountered.

What was once waste in the low metal price environment is now ore.

In the US$1350/oz gold and $17.47/oz silver scenario, the Delamar pit would process 46,734,000 tonnes at 0.34 g/t gold and 19.14 g/t silver and have a strip ratio of 0.67.

Additionally, the Florida Mountain pit would process 53,142,000 tonnes at 0.47 g/t gold and 11.83 g/t silver and have a strip ratio of 1.25.

Conversely, if you consider today’s metal prices, US$1700/oz gold and $22.00/oz silver, the tonnage at the Delamar pit increases to 51,474,000 tonnes at 0.33 g/t gold and 19.76 g/t silver and have a strip ratio of 0.92.

Florida Mountain’s tonnage increases to 59,396,000 tonnes at 0.46 g/t gold and 11.69 g/t silver and have a strip ratio of 1.39.

NOTE: These figures can be found on pages 177 and 179 of the 2019 PEA.

In total, the higher metal prices, in terms of ounces, account for a further 35Koz of gold + 4Moz of silver from the Delamar pit, and 77Koz of gold + 2.1Moz of silver, bringing the grand total to 112Koz of gold and 6.1 Moz of silver.

Those aren’t earth-shattering numbers, but still contribute to the bottom line of the project.

Putting it altogether, I like the base case scenario for the project and, outside of exploration upside, which we have yet to discuss, I like how the project responds over a variety of metal prices.

#1 – Expansion of the Florida Mountain Deposit

As I explained in my thoughts on M&A, size matters.

While comparatively, the Delamar project is already large, an expansion of the resource would be highly advantageous for its economics and appeal to major mining companies.

As you can see in the image below, there’s a large gold in soil geochemical anomaly which surrounds the existing deposit.

Integra will be targeting oxide/transitional mineralization in this area.

As investors, we should be looking for assay grades around that which we have seen on the existing deposit resource, so roughly 0.5 g/t.

While this isn’t the flashy high grade stuff Integra will be exploring for at other targets, remember that it’s oxide/transitional mineralization which is the backbone of the future operation.

The drilling of this anomaly will occur this year and, in my view, represents a tremendous opportunity to add value to the project.

#2 – Underground Resource

As I mentioned in the project introduction, the Delamar project was a past producing mine, both open pit and underground workings.

The underground workings at Florida Mountain are extensive, stretching over 2km, and will be the focus of high grade exploration this year.

In my discussion with management, these workings were encountered during the metallurgical drilling last year and returned some great intervals.

For example:

Although this high grade mineralization is underground, it appears as though it’s easily accessible and, of course, is in close proximity to the future mill site.

Outlining a high grade underground resource at Florida Mountain, therefore, represents a tremendous opportunity to add value to Delamar’s NPV, especially if the high grade material can be mined early on in the production schedule.

#3 – War Eagle

In Q4 of 2019, Integra drilled their War Eagle target, which sits roughly 3km southeast of Florida Mountain.

As you can see in the image below, they hit some very nice high grade intervals.

Given its proximity to the main project, it’s reasonable to think that at some point, depending on a number of factors, War Eagle could become a high grade production source for the mill.

A feed of high grade ore from this potential satellite deposit would be gravy on top of what already looks like a profitable operation.

Drilling at War Eagle will commence within the next 2 to 3 weeks.

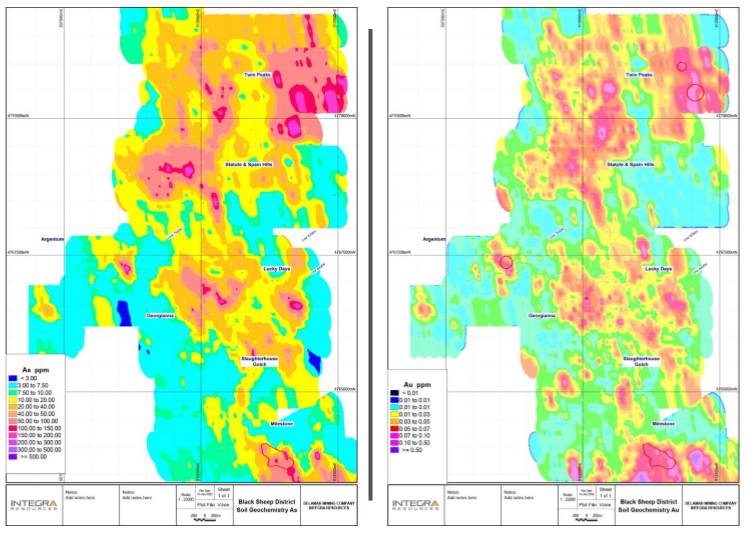

#4 – Black Sheep

Finally, there is the Black Sheep target area, which sits to the northwest of Florida Mountain.

At Black Sheep, Integra has a 25 square kilometre target area, with multiple geochemical and geophysical anomalies to follow up on.

Integra plans to drill 3,000m in this area later this year.

Exploration – The Delamar project has tremendous exploration potential across its 4 main target areas: the oxide/transitional geochem anomaly at Florida Mountain, the high grade underground target at Florida Mountain, War Eagle and, finally, Black Sheep.

With that said, with exploration comes risk.

If mineralization is intersected, what is the grade? At what depth was it discovered? Is there enough of it? All these questions need to be answered before any discovery can be deemed economic and, therefore, a positive addition to a future mine plan.

Covid-19 – The contagion of the Covid-19 virus remains a risk to every junior mining company. Any future lock down could put Integra’s action plan in neutral and, therefore, delay Delamar’s development. With a high burn rate, G&A + development/exploration costs, time not spent developing the project comes at a high cost to investors.

Gold Price – At this point, the gold price is arguably the biggest risk to company valuations, as a fall back to US$1350/oz, I believe, would result in a massive sell off and, thus, dramatic drops in company valuations.

Much like Covid-19, however, downside risk associated with the gold price is an ubiquitous risk across the sector.

With gold holding, more or less, at US$1700/oz for many weeks now, I believe it’s less and less likely that we see US$1350/oz gold any time soon.

Time will tell.

Integra’s Delamar project is excellent, it has robust economics at US$1350/oz gold and, more importantly, its sensitivity to the metal prices allows it to respond very positively to the rising gold and silver price environments that we see today.

Protecting your downside risk is integral to success in the junior resource market.

With that said, in terms of company valuation, Integra is well known within the sector and, therefore, with reference to Delamar’s base case valuation, doesn’t present a huge discount to value, in my view.

However, when you consider the exploration potential and, if successful, the impact it will have on the economics of the project, I believe this is where the true upside potential lies.

In my opinion, Integra’s story is as much about exploration as it is about development.

To add, Integra is run by a stellar group of people, who have a history of success in developing companies into premier M&A candidates.

I’m very confident that Salamis and team will continue to make the right decisions as the Delamar project continues to grow and take shape in this very important exploration season.

A PFS is expected in the second half of 2021; the discovery of further high grade mineralization could further separate Integra from the other gold development companies in Tier #1 jurisdictions.

Get the e-book Junior Resource Sector Investing Success: The Risks, Rules & Strategies You Need to Know today, when you become a FREE Junior Stock Review VIP .

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review Premium

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with Integra Resources (ITR:TSXV). I do own shares in Integra Resources.

NOTE: This update article was first published for Junior Stock Review Premium readers on May 22nd, 2020. Subsequently, FPX’s share price has appreciated roughly 30% since. Become a  today and get my best investment ideas, market commentary and interviews first.

The attention of the market right now is rightfully focused on gold and silver, as the thesis for owning the metals has never been clearer.

Conversely, base metal prices have fallen off and are at multi-year lows. The downside risk, at least in the short term, is clearly evident.

While many base metal operations have been shut down due to the Covid-19 lockdown, it’s the demand side of the equation which I think poses the most risk to the short-term future of base metals’ prices.

In my view, much of the next 3 to 6 months is still murky, as it’s unclear to me if all the quantitative easing (QE) and low interest rates will be able to stave off the impact of the Covid-19 pandemic.

To add, even if a depression-like scenario is averted, it’s my view that this global shutdown will come at a price.

That price could come in a number of forms, but the one that I think is most likely is one of stagflation.

Stagflation is defined as,

“persistent high inflation combined with high unemployment and stagnant demand in a country’s economy.â€

Although a stagflation environment paints an ugly picture for the economy and by extension base metals, I’m still very bullish on their long-term future.

I, therefore, believe any potential weakness in share prices as great buying opportunities for those who have an investment horizon of at least 1 to 2 years down the road.

Conversely, if you can handle the risk and are able to find a well-financed junior base metal explorer, discovery can pay no matter where you are in the cycle.

Today, I would like to give you an update on FPX Nickel Corp. (FPX:TSXV).

As the name suggests, FPX is a junior nickel company that is developing their Decar Nickel District in Central British Columbia, Canada.

MCAP – $24.5M

Shares – 163.3M

FD – 178.9M

Cash – $1.9M as of May 1st, 2020

Currently, FPX is focused on an updated PEA, which I believe should be dramatically different from the one released in 2013.

What’s changed over the last 7 years? A lot.

Let me take you through what I see as the major positive differences between the old and the new.

Covid-19 Crisis – While I’m citing Covid-19 as a risk, it’s really only a catalyst for supply and demand destruction and ties into the stagflation theme which I explained in the introduction. Longer term, though, FPX is at the top of my list in terms of junior nickel companies, and is currently the only one I’m invested in.

Nickel Price – It’s my guess that FPX will target a nickel price of around US$7.50/lb in their updated PEA, which means that the nickel price has to increase by almost 50% from its current price. Without an increase in price, the value of Decar is very speculative. To contrast that, take a look at the majority of undeveloped nickel projects worldwide. You will soon see that they are uneconomic at US$5.60/lbs. In fact, many require much more than US$8/lb to be economic, making FPX’s Decar very attractive.

CAPEX – There’s no getting around the fact that this will be a multi-billion dollar development project. To some, they won’t be able to see passed this, but I would point out, there aren’t many 30+ year mining projects that don’t require large upfront capital costs.

Debt – FPX does have a good chunk of debt, roughly $7.9M, however, it isn’t due for a few years and it is all held by 2 of the company’s largest shareholders. My guess, if FPX hasn’t been bought out before the loans’ maturity, FPX’s CEO Martin Turenne will find a way to eliminate it or extend the debt into the future.

In my opinion, FPX Nickel is the best junior nickel company in the market. Putting it all together, the investment thesis is as follows:

Investment in FPX isn’t without risk, but at its current MCAP, it’s trading at a fraction of its value. I continue to hold my shares of FPX and will continue to add to my position moving forward.

Further reading and watching on nickel and FPX Nickel Corp.:

2019 Cambridgehouse VRIC Presentation – https://staging.juniorstockreview.com/nickel-a-short-and-long-term-outlook/

2019 Cambridgehouse VRIC Panel – https://staging.juniorstockreview.com/junior-stock-review-nickel-panel/

Mining Stock Education – https://www.youtube.com/watch?v=AxgbpO0vebk

Original Investment Thesis Article January 2018 – https://staging.juniorstockreview.com/fpx-nickel-corp-undervalued-pure-nickel-play/

FPX Metallurgical Improvements Update – https://staging.juniorstockreview.com/fpx-nickel-corp-update-on-the-baptiste-deposit-metallurgy/

Get the e-book Junior Resource Sector Investing Success: The Risks, Rules & Strategies You Need to Know today, when you become a FREE Junior Stock Review VIP .

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review Premium

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with FPX Nickel Corp., I do own shares in FPX Nickel Corp and am therefore bias.

NOTE: This site visit report was sent to Junior Stock Review Premium subscribers on Mar.15th. Get my insights first by becoming a Junior Stock Review Premium subscriber today and save 40% using the promo code PREMIUM, until March 31st.

There is nothing like a site visit to gain perspective on a junior resource company which is moving their project towards a PFS or FS.

You just can’t beat getting a physical perspective on where a road may be built, or the mine’s proximity to a community, or where a tailings facility will be located.

Seeing the lay of the land is an X-Factor.

Additionally, it gives you the chance to spend time with management in a less formal way.

Meeting someone at a conference, at a booth, you are typically seeing a façade.

Breaking bread, having a drink or simply travelling together is a great way to see people for the way they really are.

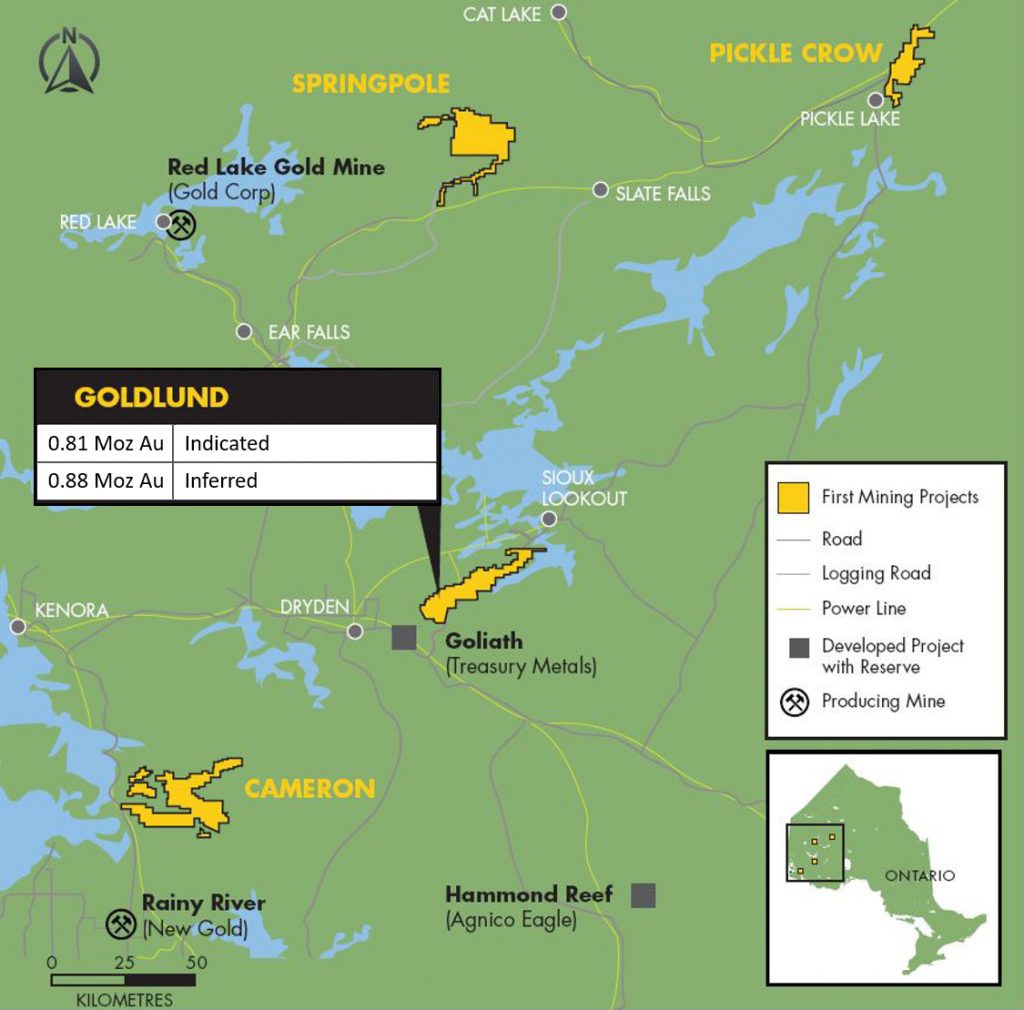

This past week, I had the chance to travel to northern Ontario, specifically Sioux Lookout, to see First Mining Gold’s Springpole and Goldlund projects.

First Mining’s land bank strategy, which the company was founded on, is gone.

A new management team, led by CEO Dan Wilton, is in, and with them, have brought a renewed focus on the development of their best projects.

In short, I will not be adding First Mining Gold to the Junior Stock Review Premium Portfolio.

While I do see value in owning the company at its current share price, I think that the risk to reward profile of the company isn’t good enough to make its way into the portfolio at its current valuation.

There are other companies that have better upside potential and less risk associated with them.

With that said, I have put together my thoughts on First Mining Gold for you here.

Enjoy!

MCAP – $107.6M (at the time of writing)

Shares – 633M

FD – 722M

Strategic Ownership – Management 3.3%, First Majestic 2.3%, Institutional 7%

Cash – roughly $12M after recently closed $8.5M financing at $0.22 and a 3 year ½ warrant at $0.33

After being away from home at PDAC the week previous, I decided to forego a hotel the night before my 8:20am flight to Thunder Bay.

It was great to sleep in my own bed, but waking at 3am to drive to Toronto’s Pearson International Airport was tough – especially with the time change the night before!

From Thunder Bay, I took a small jet operated by Bearskin Airlines to Sioux Lookout.

Sioux Lookout is a key location in northern Ontario because it’s home to one of the major hospitals – Meno Ya Win Health Centre.

Next to health care, I’m told the other major draws to the area are forestry, construction, mining and one of my favourite pastimes, fishing.

Upon landing in Sioux Lookout, I was picked up by a representative of First Mining Gold and brought to the Goldlund project.

The Goldlund property has good infrastructure with a main office building, a few maintenance structures, a large core shack and 2 core storage facilities.

Historically, Goldlund was host to an underground and open-pit mine between 1982 and 1985. In fact, the mine’s old infrastructure is still around today, with the main office building being one of the historic structures.

Goldlund is an advanced exploration project which encompasses 280 square kilometres and has a current 43-101 compliant resource on it.

Indicated Resource – 12.8Mt at 1.96 g/t for 809,200 ounces of gold.

Inferred Resource – 18.3Mt at 1.49 g/t for 876,954 ounces of gold.

Prior to First Mining, Goldlund was owned by a private company, Tamaka Gold Corporation. This changed in 2016, when Tamaka was absorbed by First Mining.

In December of 2019, First Mining closed a flow through financing at $0.27 per share. I was told by management that this money will be used exclusively at Goldlund for mostly infill drilling on its main deposit.

After lunch on Day 1, we had the chance to have a Q&A with Goldlund exploration geologist, Andrew Wiebe. Wiebe outlined the geology of the project and gave us an overview of its exploration potential.

I was particularly intrigued with the discussion over the exploration targets: Miller prospect, Camreco South and the Mustango target.

First Mining is concentrated on converting the inferred portion of the resource into the indicated category, which should be straightforward considering it is an intrusion-related deposit and makes sense from a corporate point of view.

First Mining can afford to risk capital to exploration drilling given the market and their current MCAP. Money needs to be spent on straightforward valued-added actions.

Clearly, however, there is potential outside of Goldlund’s main deposit, making the project even more attractive than it is already, considering its size, grade and location.

After discussing high level points for the project, we visited the core shack and drove to the drill rig which was set up on the Main deposit for infill drilling.

As you can see, Goldlund’s core has visible gold (VG), which is always exciting to see.

Day 2 started early, with a quick 6:30am breakfast.

Once finished, we were headed straight to the airport, where we caught an eight seat Cessna Caravan which flew us to the Springpole project.

The flight was roughly 50 minutes long and we landed on the frozen Springpole lake.

Upon landing we headed straight for the camp’s cafeteria where they were set up for the Springpole presentation, covering the mine plan outlined in the updated PEA, and the improvements that they were looking to make heading into the PFS.

After going through the project’s high level points, including a good briefing from First Mining’s David Mchaina, VP of Environmental and Sustainable Development, we jumped in a helicopter to get a good look at the lay of the land.

Specifically, for me, this gave a good perspective of the location of the proposed coffer dams and tailings facility locations.

In retrospect, I wish I had more time at Springpole to really take it in and ask more questions, but we were on a tight schedule.

I will cover more of Springpole in the following Risks to the Investment section, and following that, in my valuation metrics.

Investment in First Mining is not without risk. Here are what I believe are the biggest risks:

Time is money.

As I mentioned in the overview of the project, a bay on Springpole lake will have to be dammed and drained to allow for the open pit to be mined.

Not only this, but the planned tailings facility is almost completely surrounded by water.

These are very real risks to the environment, which will have to be clearly addressed and explained to the Federal and Provincial governments, plus eight First Nations’ communities.

Management explained that they plan to submit one Environmental Assessment document to both the Federal and Provincial governments for simultaneous approval.

Also, the company is considering incorporating the use of a synthetic tailings liner and dry stack tailings into the PFS mine plan.

This will no doubt come at a higher cost, but will give themselves the best possibility of being approved.

Further, it should be noted that the damming of the lake for the construction of an open-pit mine isn’t unheard of in Canada.

Examples are Agnico Eagle’s Meadowbank gold mine and Rio Tinto’s Dvavik Diamond mine.

Permitting is going to be a long process and could be a hindrance to value recognition from the market.

Or, maybe the market will turn bullish and permitting risk won’t matter to a portion of investors.

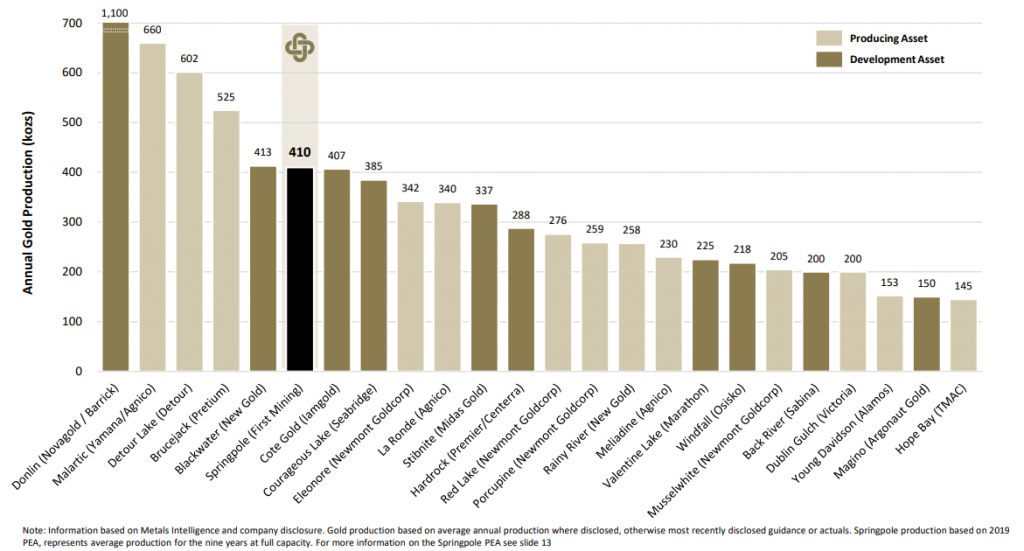

At first glance, this seems very high, however, remember that Springpole is expected to produce roughly 400,000 ounces of gold per year – this is rare. Given other large undeveloped gold projects of similar size, the cost, from what I can tell, is in line.

Consider the following graph provided in the First Mining Corporate presentation:

New Gold’s Blackwater is estimated to cost $1.8 billion to construct, Iamgold’s Cote Lake is estimated at $1.5 billion, Seabridge’s Courageous Lake US$1.52 billion, Midas Gold’s Stibnite is $1.12 billion and Sabina’s Back River is $476 million (but it is half the production).

My point is, although the CAPEX to construct Springpole will rise, in my view, costs will still be in a range which is in line with other large projects.

With that said, Springpole will have to rely on other factors to make it stick out from the crowd.

Other factors could possibly be location, mine life, exploration potential or AISC.

$3.5 million in G&A is a lot and is rarely justified in my books. Management teams that are making this kind of money usually have share price charts that move in the opposite direction of First Mining.

Examining the chart, you can see that over the last three to four years, shareholders have been delivered nothing but losses and dilution.

Conversely, good people demand top dollars, which I won’t argue with. Given that First Mining’s new team has only been around for a year, I think that they deserve a chance to deliver on their vision.

From what I can tell, the right people are now leading the company.

I haven’t met CEO Dan Wilton, but in asking around, he does have a good reputation.

Second most important is COO Ken Engquist.

Engquist is a technical guy with a very relevant skill set and resume.

Personally, having heard Engquist’s pitch on the path of the company, I’m interested to see how they develop their portfolio of projects over the next year.

With that said, it only goes so far.

As I mentioned, with a $5M per year burn rate outside of value-added work, they will be coming back to the market most likely before the end of the year.

Further, if First Mining were to finance under $0.22 in the future, I would consider it a colossal failure.

As I said, I will not be adding First Mining Gold to the Junior Stock Review Premium portfolio.

With that said, I will be following the share price, as there may be opportunity to add it to the portfolio if the share price were to fall further.

You will be alerted if I change my mind.

To close, this is how I break down the value opportunity in First Mining Gold:

The fact is, there are just not many development projects like this.

At US$1500/oz gold, Springpole’s after-tax NP@5% is US$1.22 billion with a 28% IRR. Let’s assume that Springpole’s value is 10% of its NPV, which is, therefore, US$122 million. With the current USD to CAD exchange rate that is roughly $168M CAD.

The company has a MCAP of approximately $107 million CAD. Conservatively, there is almost 70% upside in the share price just in considering Springpole, never mind the other projects.

Because of this, Goldlund is easily the best bargaining chip First Mining has to play with moving forward.

Treasury Metals’ Goliath project is located in close proximity and shares some commonalities as far as I can tell. Many analysts that I know believe that Goliath and Goldlund should be in the same company at some point in the future.

However, we probably need a better market to make this happen.

For now, I think that assigning a value equal to Treasury’s current market valuation makes a lot of sense.

At the end of trading on Friday March 13th, Treasury’s MCAP was roughly $30M.

In terms of valuing the JV agreement, I will discount the $3 million spend over the next 3 years and say it is worth $2 million. This only assigns value to the spend, no value to the project.

Putting it all together, First Mining Gold is trading at half of its intrinsic value, conservatively speaking.

While this gives us as investors plenty of downside risk protection, given the risks associated with the company, I believe there are better places to invest our money.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review Premium

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with First Mining Gold, however, they did, along with Soar Financial Partners, pay for most of my travel expenses.

NOTE: This interview was completed on Feb.21th, 2020 and was published for Junior Stock Review Premium subscribers on Feb.24th. Become a Premium subscriber now and save 40% by using the Promo Code PREMIUM by March 31st.

I first wrote about Aethon Minerals in the spring of 2019, when it was trading at roughly $0.125 per share (Or $0.033 per share of AbraPlata Resources post merger).

Aethon had just announced that they struck a deal with AbraPlata Resources, which would give them the exclusive right to perform technical due diligence over a 5-month period on AbraPlata’s Diablillos silver-gold project in Argentina.

Fast forward to September 4th, 2019, around the time of the announcement of the definitive agreement between the two companies, and I wrote a full article outlining the investment thesis.

Currently, AbraPlata is trading at $0.11, making it a triple for readers and myself. Even today, with a MCAP of close to $30M, I still believe that AbraPlata is undervalued, especially when you consider their latest drill results – this is a rich epithermal system.

Why is it still undervalued?

In my view, it’s solely based on Diablillos’ location – Argentina.

Jurisdictional risk should be a major part of any junior resource sector investor’s investment analysis. Understanding the risks of a particular jurisdiction can be helpful in understanding why a certain company’s MCAP is discounted.

Jurisdictional risks can range from political instability, to a lack of rule of law or potentially any number of environmental concerns which today, seemingly, can become an issue or risk anywhere on the planet.

In my view, it’s ultimately the culture of the people who live in the country who dictate how the country conducts itself.

For example, the people of Ecuador have major ties to the rainforest and the environment in general. Thus, I believe, they will always pose some sort of risk to mining. Now, I’m not saying this is right or wrong, just that in terms of mining companies, you must realize that this social issue isn’t going away.

Cultures take hundreds of years to form and hundreds of years to change. Therefore, what you see is basically what you get.

In saying this, reading about a culture can only get you so far in terms of understanding it. In reality, I think that you need to live in a country for a period of time to really get a real feel for the culture and how it ticks.

With this said, today I’m sharing a conversation with David O’Connor. O’Connor is Chief Geologist with AbraPlata Resources (ABRA:TSXV) and has over 40 years of experience in mineral exploration.

Most importantly, O’Connor has called South America home for 27 years having first lived in Bolivia, then Chile and now, most recently, Argentina.

Let’s hear what O’Connor has to say about Chile, Argentina and of course, AbraPlata’s flagship project – Diablillos.

Enjoy!

Brian: You have a lifetime of experience within the mining industry with over 40 years to date. I think it is safe to say that you have experienced every facet of mineral exploration and, of course, the nuances of exploring for mineral deposits beyond the confines of the country you were born in.

For context, can you give us a little bit about your background – education, where you got started in the mining industry, where you have lived, etc.?

David: I did my undergraduate degree at Cape Town University, then worked in the Messina copper mine in South Africa for a year before moving to Australia where I worked for several years with Western Mining Corporation. I took time off to complete my Master’s degree in Mineral Exploration at the Royal School of Mines in London, following which I returned to Western Mining, ending up in charge of exploration in South Australia, where we discovered the Olympic Dam deposit.

I then moved to Peko-Wallsend (Geopeko) where I became their chief geologist. Later, I moved to France, where I established a subsidiary of Nicron Resources, which was an Australian lead-zinc miner. We explored the old lead mines in France and Belgium for their zinc content. I then wrote a multi-client study called “Development Opportunities in Lesser Developed Countries” and decided to move to Bolivia, where the World Bank was assisting with privatisation of state mining projects.

In Bolivia, Ross Beaty (old friend from the School of Mines) and I established two junior exploration companies, the first being Da Capo and the second Altoro. With Da Capo we developed resources to the feasibility stage on two mining areas, the main one being Capacirca. We merged Da Capo with a mining company called Granges, to form Vista Gold. With Altoro we concentrated on a platinum-paladium project in Brazil, on the strength of which we merged with Solitario Resources.

I moved to Chile when things went ethnic in Bolivia and established Explorator Resources, with which we developed the El Espino IOCG resource to feasibility stage and sold it to a local copper miner called Pucobre.

I joined Aethon Minerals in 2018 and moved to Argentina a couple of months ago when Aethon merged with AbraPlata. I now live in Salta, which is conveniently close to the Diablillos silver-gold project.

Brian: I’m particularly interested in hearing more about your time in South America. Starting with Chile, in your opinion, why do most mining people continually rate it as the best place to do business in South America?

David: Chile is well endowed with mineral resources, with the porphyry copper deposits there supplying roughly a third of the world´s copper, together with substantial gold and other metals, more recently including lithium. Mining is very important to the Chilean economy and has become so because of the government´s policies, which have attracted the needed foreign investment to explore and develop the mines. The country is advanced regarding infrastructure and services, even though the exploration areas in the high Andes mountains can be challenging.

Brian: AbraPlata has a few JV ready projects in Chile, one of which has a great JV agreement with Rio Tinto.

Can you give us an outline of these projects and their potential?

David: The Arcas mineral rights block, on which Rio Tinto has entered into an agreement, is located in the porphyry belt north of the mining city of Calama, which services the major porphyry copper-gold mines in the area. The Arcas block has outcropping porphyritic intrusions, together with the relevant anomalous geochemistry to host copper-gold deposits. However, exploration in the relatively remote area is more appropriate to a major company with the finances to handle it, which is why we joint ventured it to Rio Tinto.

Brian: There is great potential in AbraPlata’s Chilean projects, but the main attraction or pillar of the investment thesis in AbraPlata revolves around the Diablillos project, which is located in the Salta Province of Argentina.

Having now lived in Argentina for a few months, what would you say are some of the differences between living in Chile and living in Argentina?

Do you see there being a correlation between those differences and the mining investment attractiveness of each of the countries? Please explain.

David: As mentioned, I live in Salta, which is a delightful little city in Northern Argentina, convenient to the Diablillos project and well serviced with flights to Buenos Aires etc. Argentina has had its political challenges in the past, but the new president has stated his support for the mining industry, realising that attracting foreign investment is an important means for supporting the economy. In Argentina, each province has its own minerals policy, with certain provinces being more pro-mining than others. It is important to note that mines and mineral exploration in the pro-mining provinces has continued through several changes of federal government.

Brian: Unlike Chile, Argentina has a stigma for being one of the riskier jurisdictions to invest in within South America. To a certain extent, I can’t disagree, as politically there have been some major gaffs over the last 20 years.

However, in terms of mining law and regulation, Argentina is different than most of the other South American nations, because it’s governed at the provincial level.

With that said, Salta province has a good history and reputation as being a stable region for operating mining companies.

From lithium brine operations to other hard rock mining projects, there is a lot going on in Salta.

Can you give us more context as to what is going on in Salta right now? Are companies moving forward with their projects?

David: Salta province is particularly pro-mining and the provincial government recognises it as an important source of income for the province. As well as the historic borax mines and the more recently developing lithium mines, Salta hosts the major Taca Taca copper porphyry and the Lindero mine which is currently being constructed not far from Diablillos. We are in a mining friendly environment.

Brian: Having just gone through the process of getting drilling permits and the other work that goes into developing a mineral exploration project recently, how did you find the process?

David: Fortunately for us at Aethon, when we merged with Abraplata, that company was very well prepared regarding permits, community relations etc. And we were able to move immediately into drilling at Diablillos. I think AbraPlata is competently represented with its legal and administration team, who pay close attention to legal and community issues. Having recently met with the new Secretary for Mines and Energy for the province, who ensured us of his department´s continuing support, I feel confident that we will be able to proceed smoothly to develop and expand resources at Diablillos.

Brian: You have touched on a lot of positives, but there is always risk.

Where do you see the potential risk for exploring and developing a mineral project in Argentina?

David: Frankly, I think that there is undue concern about potential risks in the mining friendly provinces, but that is not the case in provinces, or parts of these provinces, where agriculture and tourism compete for space. In these mining will always be up against local community issues. An overall concern, if you insist on looking for one, is if the Federal government might consider raising taxes in the future. However, it seems that common sense will prevail and they will not kill the goose that will continue to lay bigger and bigger golden eggs.

Brian: Recently, AbraPlata released some great drill results, which were highlighted by some stellar intervals – 17.5 metres of 604 g/t silver and 7.0 metres of 20.6 g/t gold and 202 g/t silver.

Can you summarize the results and give us context as to how it fits in with the overall geological model of the Oculto deposit?

David: The Oculto deposit is a high sulphidation epithermal system which hosts silver and gold resources that were the basis for a robust PEA on an open pit project. However, a preliminary desktop study by RPA indicated that an underground mining scenario could potentially be attractive, because of substantially lower initial capital cost (no pre-stripping, smaller plant etc.), rapid payback time and better metallurgical recoveries due to a higher head grade. While this study remains preliminary at this stage, the main objective of the current drill program is to expand the deeper gold resource and then complete additional work which would enable us to release a new optimized PEA, planned on an underground mining scenario.

We decided to drill a bit deeper than previous campaigns and have intersected substantial copper sulphide mineralisation beneath the oxide gold and silver resources, with associated gold and silver with the copper in places, as announced this week.

Brian: Outside of the Oculto deposit, are there any other targets of interest? Please explain.

David: Outside of the Oculto silver-gold deposit in the shallower oxide zone, a new target is the underlying copper and precious metal Zone beneath it in the sulphide zone.We will keep chipping away at this with our current drilling program, as we drill to expand the overlying oxide gold resource. The breccia zones hosting sulphide mineralisation at Oculto are probably related to outcropping breccias in the Cerro Viejo and Cerro Blanco areas within the Diablillos project area, where they are related to outcropping porphyries. These are additional targets which I plan to explore in due course.

Brian: Thank you very much for your time and your views, it’s much appreciated!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review Premium

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with any of the companies discussed in this article. I do own shares in AbraPlata Resources.

Mr. Market never disappoints, the cycle between market darling and bottom dweller is continuous and really doesn’t discriminate – everyone is afflicted at some point. The key is to find the companies that are currently bottom dwellers, but truly deserve to be valued as market darlings.

More on this point, a few years ago, while attending a resource sector investment conference, I heard Rick Rule say, and I’m paraphrasing,

“In the short-term, the market is a voting machine and in the long-term, it’s a weighing machine.”

Rick Rule

In my view, Rule is saying that in the short term, Mr. Market is more emotional and swings with the popular vote, so to speak. In the long term, Mr. Market is more calculated and quantitative in its approach and, therefore, allows each company to attain their intrinsic value – good or bad.

Today, I have for you some comments on a sector and, more importantly, an investment thesis on a company which I believe is tremendously undervalued. The sector is zinc and the company is Fireweed Zinc.

Let’s take a look.

One of the hottest metals markets to be invested in over the last 5 years has been zinc. From its low in late 2015, to its high in early 2018, the zinc price more than doubled and, with it, brought a ton of attention to the junior zinc companies.

The zinc price strength was derived by supply constraints as a number of mines and smelter facilities closed or had their production suspended.

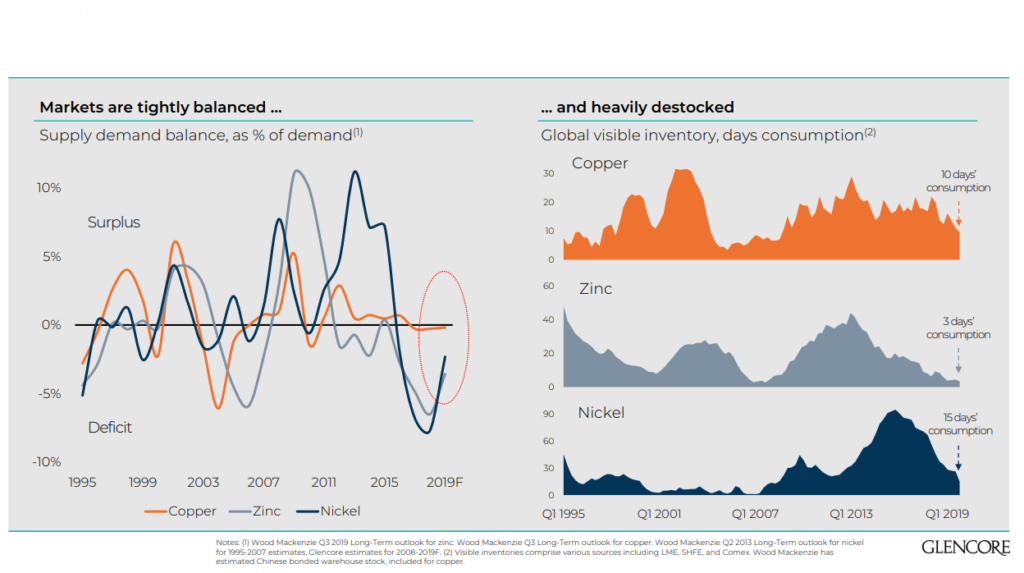

Glencore has a great graph, in their most recent corporate presentation, of the current global metal inventories of copper, zinc and nickel. All of which remain low, zinc in particular sits at 3 days of consumption – which, I think, many would equate with price strength, not weakness.

Today, however, the zinc price has fallen drastically from its highs above US$1.50/lbs and is sitting at roughly US$1/lbs.

This major fall in the zinc price has brought many of the junior zinc company share prices with it, and I believe it gives investors a great buying opportunity, if you choose wisely.

MCAP – $20.7 million (at the time of writing)

Shares – 37.7 million

FD – 44.7 million (only a small amount of warrants outstanding)

Cash – roughly $1 million

Ownership – Management – 19%, TECK – 10%, Hudbay – 10%, RCF – 13%

NOTE: Teck was the lead order in the $5 million private placement early in 2019, purchasing 2.1 million shares for an investment of $1.75 million. Also, RCF topped up their position purchasing $750K worth of shares.

So why invest in Fireweed Zinc?

Besides a tight share structure and good strategic ownership, I think investment in Fireweed at its current MCAP comes down to 2 main points: its people and project.

First and foremost, the investment thesis starts with CEO, Brandon Macdonald. Brandon is a geologist by trade and has a very good educational background with an MBA from Oxford. Now, I don’t personally know Brandon as well as I would like to, but I do have a couple of friends that know him very well and speak very highly of him – which is good enough for me.

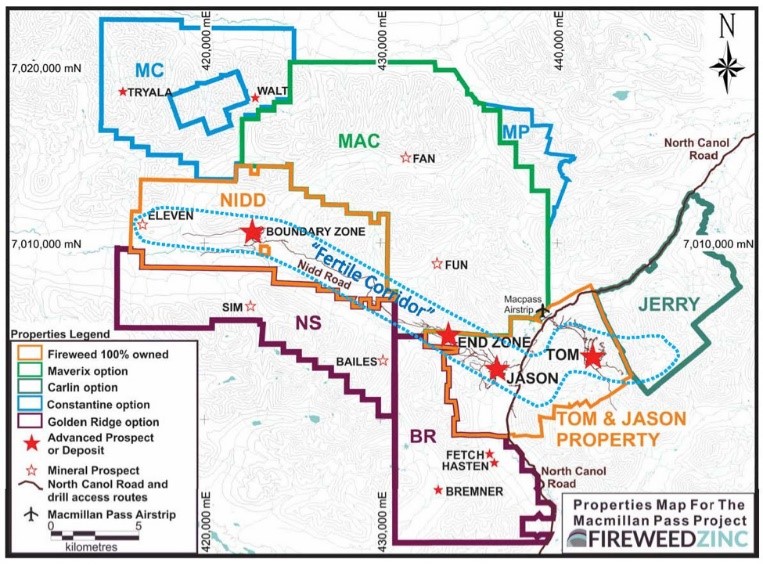

Additionally, in my opinion, the fact that Brandon is from the Yukon or, more specifically, Ross River, I believe this is an X-Factor and something that will pay huge dividends in the future.

Another important factor in the Fireweed story is its association with Discovery Group. In fact, co-founder and principal at Discovery Group, John Robins, is the Executive Chairman and brings a history of success in the Yukon, ie. Kaminak Gold, and an extensive rolodex which opens doors to both capital and technical knowledge.

I believe that Fireweed is undervalued considering the quality of its assets – MacMillan Pass Project. I say this, however, I must add the caveat that the MacMillan Pass Project is not economical at the current metal prices given their 2018 PEA.

To start, let’s take a look at the 2018 PEA figures for perspective:

After-tax NPV@ 8% – $1.1 billion

After-tax IRR of 24%

Pre-Production CAPEX – $404.3 million

Open Pit / Underground Mine

Mine Life – 18 years

Payback – 4 years

Indicated Resource – 11.2 Mt: Zinc 6.59% – 1.63 billion lbs, Lead 2.48% – 0.61 billion lbs, Silver 21.33 g/t – 7.69Moz , Zinc Eq. 9.61%

Inferred Resource – 39.5Mt: Zinc 5.84% – 5.08 billion lbs, Lead 3.14% – 2.73 billion lbs, Silver 38.15 g/t – 48.41 Moz, Zinc Eq. 10.0%

Assumed metal prices – Zinc US$1.21/lbs, Lead US$0.98, Silver US$16.80/oz

These are some great numbers and really separate the MacMillan Pass Project from the rest of the pack of other undeveloped zinc projects worldwide.

It starts with the size of the Tom and Jason deposits, which have a combined indicated and inferred resource of over 50 Mt.

The impact of having such a large resource has a trickle-down effect on the rest of the important aspects of the project and, most importantly, I think, allows for a long mine life, giving a would-be buyer the chance to be right about the economic viability of the project over its lifetime.

One of the issues of a shorter mine life is that they have to be developed at the proper time or they risk being ready or in production, over the majority of their life, during a metal price environment which is uneconomic.

There are a couple of size comparisons for Fireweed, but each is valued much higher by the market. Now, not every pound or ounce of metal is created equal, I totally agree. In this case, however, I think the market has it wrong.

If you do your research on the undeveloped zinc companies worldwide, you will find that a large portion have completed economic studies using a zinc price between US$1.20 and US$1.30 per pound.

Therefore, you need to chose right if you’re going to invest in a zinc company, because when the zinc market does eventually come back, it’s going to be the best projects out of that grouping which are going to be acquired or developed.

So what’s going to separate the wheat from the chaff?

It could be a number of different things, from jurisdiction to upfront capital cost, to acquisition cost, to economics. The location of each project can’t be changed and, therefore, I think the best companies will separate themselves by continuing to improve their projects, by increasing NPV / IRR and, ultimately, trying to reduce the metal prices that they require for an adequate return on capital invested.

Personally, I think that zinc companies that have a silver component to their deposit stand a good chance of standing out from their peers given the outlook for precious metals in 2020.

Now, I won’t be hanging my hat on this for the basis of my investment; speculating in metal price movements is not a good reason to buy a junior resource company.

Fireweed, however, does have close to 60 Moz of silver, which is large and fairly rare if you look around the junior resource space. High silver prices could be icing on the cake to the Fireweed investment thesis, if it were to head above US$20/oz.

Thus far, all of the information regarding MacMillan has been with reference to the Tom and Jason Deposits. Another ace up CEO MacDonald’s sleeve, however, could come from the Boundary Zone.

Over the last couple of months, I have been pleasantly surprised with the drill results that have come from the Boundary Zone. They are highlighted by:

These are great results and near surface to boot. The Boundary Zone has the potential to be a real difference maker in the size and production profile of MacMillan, moving forward.

Additionally, the company is testing XRF ore sorting technology, which would, theoretically, be used in conjunction with the mining of the Boundary Zone, thus feeding the mill with high grade ore, in-conjunction with that which is being produced from Tom and Jason.

Unlike metal price predictions, I will speculate that this is going to improve the NPV of the MacMillan project and, therefore, is a big part of the investment thesis in Fireweed.

In many cases, junior resource companies have a period in which they proverbially fall from grace in the eyes of the market. In many cases, it’s warranted, as the company eventually reaches its intrinsic value of 0. In special cases, however, value investors can find a diamond in the rough.

In my opinion, Fireweed Zinc at its current MCAP is a diamond in the rough and is why I recently bought shares.

Now an investment in Fireweed isn’t without risk.

The first risk is Fireweed’s cash position. Currently, they have roughly $1 million, which is not enough to do anything highly impactful. Dilution at such a low MCAP is not ideal, but may be necessary. Personally, I would like to see Teck and RCF be lead orders in the next placement in 2020.

The second risk is the zinc price; further weakness in the price could put Fireweed into neutral. As I mentioned earlier, however, almost the whole undeveloped zinc market would be in the same boat and, therefore, I’m happy to stick with the best undervalued issuer.

Finally, I think it’s justified to be skeptical on the Yukon. It’s a great jurisdiction in many respects and there has been success with Victoria Gold now a producing gold mine. But, a large primary base metal project is a different beast altogether.

In the end, I think that MacMillan has the right location in terms of accessibility to make it work and, therefore, I think the risk is noted, but not detrimental to its development.

NOTE: See BMC Minerals, who are in the final stages of permitting their primary zinc project, which is located in close proximity to the MacMillan Pass Project.

In closing, I’m a buyer and am bullish on Fireweed.

First, because of the people. Brandon Macdonald is a smart and trustworthy man, who is at the very beginning of what I think will be a long and successful career in the mining industry.

Moreover, he is supported directly by an Executive Chairman, John Robins, who has a stellar resume from his more than 35 years in the business.

Second, I believe the MacMillan Pass project is in a class of its own, especially given its current valuation. It’s a large deposit, and given the success with step out drilling at the Tom deposit, and arguably more importantly, the great results from the Boundary Zone, I think it’s about to get a whole lot better in the future.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with Fireweed Zinc or any other company mentioned in this article. I do own shares in Fireweed Zinc.

Day 2 began at Cartier Resources’ offices in Val d’Or. Interestingly, Cartier’s office walls are filled with field work photos, Chimo mine blueprints, deposit layouts, historical Val d’Or mining statistics and a whole host of other interesting pictures.

Personally, I thought this was a nice touch for visitors as it gives a good perspective on what the company has and is doing to move the company forward – a picture is worth a thousand words.

MCAP – $30.1 million (at the time of writing)

Shares – 177.1 million

Cash – roughly $6 million

CEO – Phillippe Cloutier is a geologist by trade with over 25 years of experience in mining exploration and development.

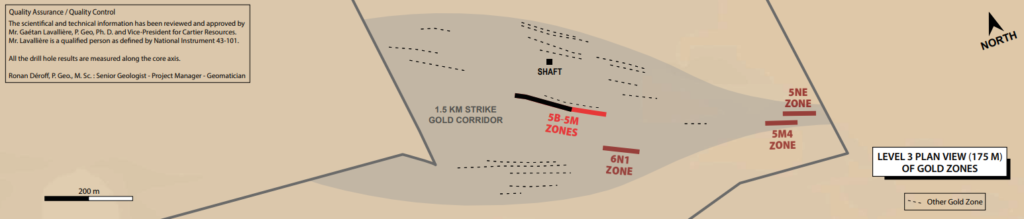

Cartier made it clear that using funds efficiently is their top priority; they started their presentation by outlining how they go about their exploration work with an added focus on how they planned their drill programs on the past producing Chimo mine property.

The talk was led by VP Dr. Gaetan Lavalliere, who is a professional geologist with over 25 years of experience in the mining industry.

Cartier organizes their geological data to formulate a prioritized list of targets. By doing this, they are always focused on the targets that have the highest probability of returning good results for each dollar spent.

With regards to Chimo, the team was focused on 3 high priority targets from the deposit’s 24 zones.

It should come as no surprise that these zone extensions are mostly at depth, which fits the Abitibi shear zone related gold deposit model. Each of the companies that we visited on our trip were focused on targeting high grade gold mineralization at depth.

I believe Osisko’s ‘Discovery 1’ hole could prove to be a major catalyst for all the other companies with gold projects along the Abitibi, to follow suit and explore deeper…much deeper.

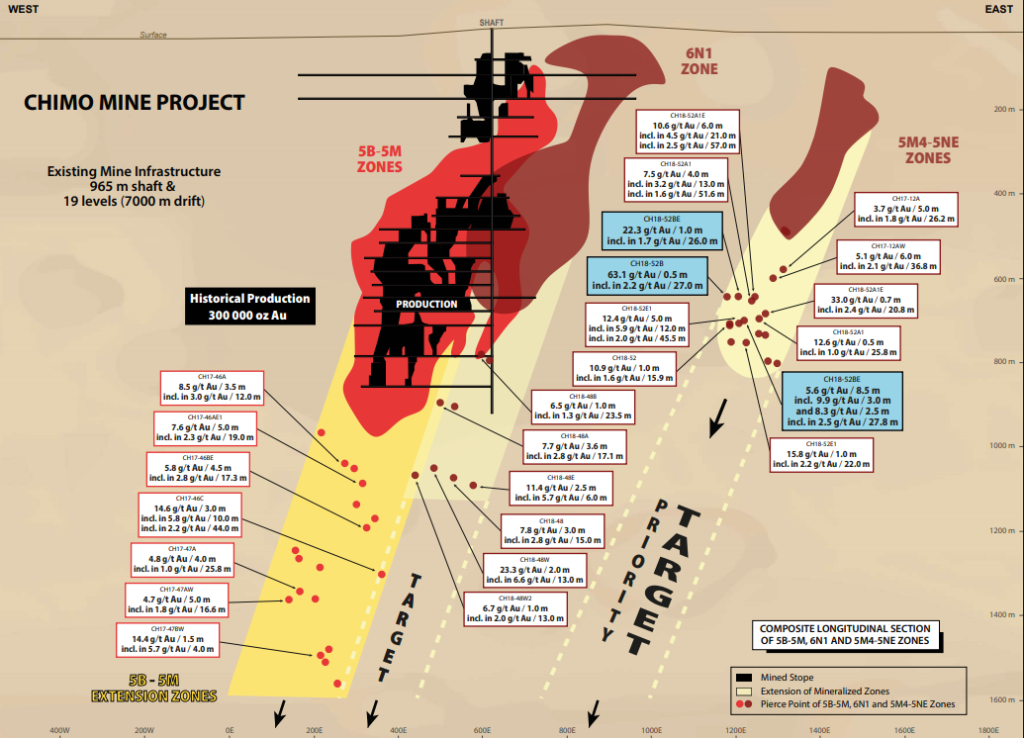

Cartier’s zone extension drilling, in my opinion, has been a success with some very good grades and widths. Reviewing the images above, which were provided by Cartier, you can clearly see how the drilling was systematically planned to delineate the gold mineralization.

If I were to have a criticism of Cartier, it would be that they don’t have any 43-101 technical reports supporting what they have done at Chimo. To explain that further, I fully subscribe to the fact that any senior company interested in Chimo will disregard any technical report Cartier possessed in favour of conducting their own due diligence.

Moreover, most sophisticated investors in the sector can review the drill results and historical mine data and construct an economic model for the revitalized mine and have an idea of its potential value.

The problem, at the moment, is the company says they are targeting the retail market, who, by and large, don’t have the necessary skills to calculate the value of Chimo. Instead, they are depending on someone else’s opinion to gauge its potential value.

NOTE: On a high level, to model Chimo effectively, you would need to have a grip on two important points; the resource size and grade and cost of dewatering the flooded shaft and underground workings. With realistic values for these 2 points, you could model the project using the costs and tax structures from other economic studies or mines in the general Val d’Or area.

In open discussion with CEO Cloutier, this point hasn’t been overlooked by the management team. They are now, however, in a position that requires them to conserve money and await a buyer for Chimo. The conservation of cash allows Cartier to weather any storm that may be headed their way when it comes to negotiation for Chimo.

Who would be a likely candidate to purchase Chimo?

That’s a great question and one that’s key to Cartier’s investment proposition.

First and foremost, the obvious candidate is O3 Mining, which, over the last month or so, has bought up a ton of land around Chimo, through their purchases of Chalice Gold Mines and Alexandria Minerals.

O3 Mining is a new company formed by the Osisko Mining team, whose track record supports an aggressive approach to all aspects of mining company development.

In my opinion, if O3 were interested in Chimo, it wouldn’t be for the short-term production capability, it would be because they see the potential for a much larger system in the area, Chimo just being one of the key pieces.

Additionally, I have heard Agnico Eagle’s name come up as a potential suitor for the purchase of Chimo. I’m less inclined to believe they are a better candidate than O3 to make the purchase, because Chimo, at this point, is much smaller in both resource size and land position than would typically entice a major’s attention.

While O3 and Agnico are arguably the top takeover candidates, it could be a much smaller producer with underground experience that is willing to take on this small short-term production capability story, but they will have to be well financed to make it happen.

Time will tell.

Personally, I do see the value in owning Cartier, even without having modelled Chimo. They are cashed up, have a good management team, and have a bunch of other high potential projects that are just waiting in the wings as far as exploration goes.

Without a doubt, there will be a buyer for Chimo, it’s just a matter of price and when it will happen.

A potential investor must realize that a deal may not be imminent and understand that Cartier will be in hibernation mode until a deal can be made. Depending on your investment outlook and level of patience, this could be a deal breaker.

Don’t want to miss a new investment idea, interview or financial product review? Become a Junior Stock Review VIP now – it’s FREE!

Until next time,

Brian Leni P.Eng

Founder – Junior Stock Review

Disclaimer: The following is not an investment recommendation, it is an investment idea. I am not a certified investment professional, nor do I know you and your individual investment needs. Please perform your own due diligence to decide whether this is a company and sector that is best suited for your personal investment criteria. I have NO business relationship with Cartier Resources, nor do I currently own any shares. However, all of my expenses for the site visit were paid for.

In the first half of 2019, most of the questions I received from readers involved the gold price and where I thought it was headed. Now, 8 months later and with the gold price surpassing US$1500/oz, the focus of the questions has shifted to the other precious metal – silver.

Silver is often referred to as gold on steroids, as historically it has outperformed gold both to the upside and downside depending on the direction of the market. Today, the silver price has eclipsed US$18.50/oz and, at this rate, may even surpass US$20/oz by the end of 2019.

The factors driving the silver price are closely related to those driving gold, mainly the FED lowering interest rates, the talk of further QE, negative interest in Europe, the turmoil surrounding the U.S. and China trade war, and the ever-increasing list of financial calamities around the world.

Additionally, silver has a component of industrial use, which I think is the added driver of its volatility.

The rising silver price has brought with it a large amount of speculative cash which is flowing into many of the junior silver companies. Reviewing my watch list, many of these companies are up by huge amounts, mostly for no reason other than they offer perceived leverage to the silver price.

It’s the classic buying of junior resource companies because of a bullish outlook for a metal. This mentality in the junior resource sector, while it may bring short-term gains, will ultimately lose money for investors over the long term.

Junior resource companies are speculations on management’s ability to execute on a well thought out plan, which aligns with their overall vision for the company. If people can’t execute, it doesn’t matter where the metal price goes, the metal will either not be discovered or developed into a mine – period.